Your Student Loan Repayment Timeline Explained

- TitanPrep Official

- May 26

- 8 min read

If you have federal student loans, knowing your student loan repayment timeline is one of the most practical things you can do for your finances. Yet most borrowers leave school without a clear picture of when payments start, how long repayment actually lasts, or what the 2026 plan changes mean for them. This article walks you through every stage of the process, from your grace period to forgiveness, so you can make informed decisions rather than costly mistakes.

Table of Contents

Key takeaways

Point | Details |

Grace period starts at graduation | Most federal loans give you 6 months before your first payment is due. |

Standard plan spans 10 years | The fixed 120-payment schedule pays off loans fastest but costs more monthly. |

Average payoff takes about 20 years | Income-driven plans extend timelines significantly beyond the standard 10 years. |

RAP launches July 1, 2026 | A new 30-year forgiveness plan replaces most income-driven options for new borrowers. |

Forgiveness may be taxable | IDR forgiveness after December 31, 2025, counts as taxable income under current law. |

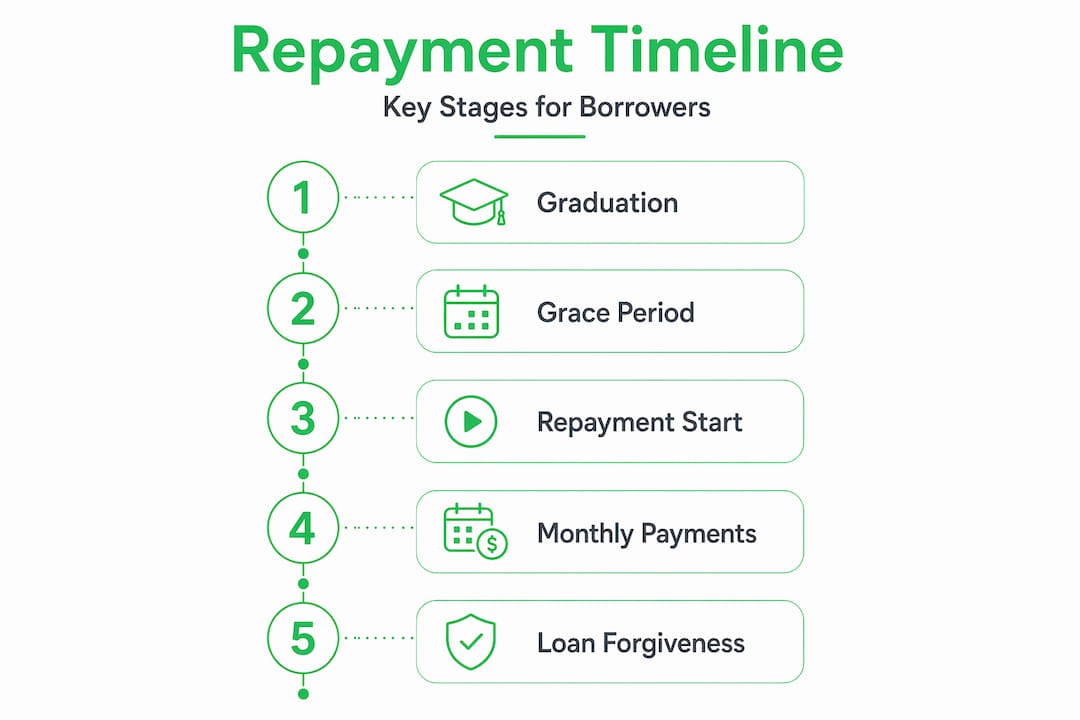

Understanding your student loan repayment timeline

Your student debt repayment timeline does not begin the moment you borrow. It begins the moment a specific trigger occurs, and that trigger depends on your loan type.

For Federal Direct Subsidized and Unsubsidized loans, repayment begins after a 6-month grace period that starts when you graduate, withdraw, or drop below half-time enrollment. This window is not just a delay. It is time you can use to find employment, set up a budget, and choose the right repayment plan.

There is a meaningful difference between the two most common loan types during this period. Subsidized loans do not accrue interest during the grace period, so your balance stays flat. Unsubsidized loans keep accruing interest from the day they are disbursed, meaning your balance grows even while you are in school and during those six months before repayment starts.

Parent PLUS loans work differently. Parent PLUS loans have no automatic grace period, and repayment begins immediately after full disbursement unless the borrower requests deferment. Grad PLUS loans, on the other hand, carry an automatic 6-month deferment that mirrors the standard grace period.

Once repayment begins, you are placed on the Standard Repayment Plan by default. Here is what the most common loan repayment schedules look like:

Standard Repayment Plan: Fixed payments over 10 years (120 monthly payments)

Graduated Repayment Plan: Payments start low and increase every 2 years, also over 10 years

Extended Repayment Plan: Stretched to 25 years for borrowers with over $30,000 in federal loans

Income-Driven Repayment (IDR) Plans: Payments based on income, with forgiveness after 20 to 30 years

The standard plan covers 120 monthly payments, but the average borrower actually takes about 20 years to fully pay off their loans. That gap exists because many borrowers switch to income-driven plans to lower their monthly payments, which stretches the total student loan payoff period considerably.

Pro Tip: If your income is low right after graduation, income-driven repayment can protect your budget. But it also means paying more interest over time. Run the numbers on both options before you commit.

What is changing in 2026 and beyond

The student loan repayment landscape is shifting significantly. If you are a new borrower or currently enrolled in an income-driven plan, these changes affect your loan repayment schedule directly.

The One Big Beautiful Bill Act, signed into law in 2025, consolidates the available repayment options. Starting July 1, 2026, the Repayment Assistance Plan (RAP) will replace SAVE, PAYE, and ICR for new borrowers. RAP features a 30-year forgiveness timeline, which is longer than most previous income-driven plans.

Here is a side-by-side look at how the plans compare:

Plan | Monthly payment basis | Forgiveness timeline | Available to new borrowers after July 1, 2026? |

Standard Repayment | Fixed amount | 10 years (no forgiveness) | Yes |

IBR (existing borrowers) | 10-15% of discretionary income | 20 or 25 years | No (existing borrowers only) |

RAP | 1-10% of total AGI | 30 years | Yes |

SAVE / PAYE / ICR | Varies | 20-25 years | No (phase-out by 2028) |

RAP calculates payments as 1 to 10% of your total adjusted gross income, without the discretionary income exemption used by older plans. There is a $10 minimum monthly payment. That structure may feel affordable now, but the 30-year forgiveness timeline means most borrowers will pay more interest overall compared to the standard plan.

A few critical details every borrower should know:

SAVE, PAYE, and ICR will be phased out for existing borrowers by 2028

IBR remains available for borrowers who enrolled before July 1, 2026

Parent PLUS borrowers are not eligible for RAP, creating a gap in repayment options for that loan type

IDR forgiveness after December 31, 2025, is taxable income, unlike Public Service Loan Forgiveness, which stays tax-free

Pro Tip: If you are currently on SAVE, PAYE, or ICR, do not wait until 2028 to act. Review your options now, because the SAVE plan repeal is already affecting borrowers.

Strategies for managing your repayment timeline

Understanding your options is the first step. Putting them to work is the second. Here are practical strategies to take control of your student loan payoff period from day one.

Use the grace period intentionally. Most borrowers treat the grace period as free time. A better approach is to make even small payments toward your Unsubsidized loans during this window. Payments during the grace period reduce the interest that gets added to your principal balance, which lowers your total repayment cost.

Choose your plan, do not accept the default. You are automatically placed on the Standard Repayment Plan when repayment begins. That plan is fine for some borrowers, but not for everyone. Borrowers with a debt-to-income ratio under 0.5 typically do well on the standard plan, while those with a ratio above 1.0 often benefit more from income-driven options. Log in to studentaid.gov and actively select a plan that fits your income and goals.

Be careful with consolidation. Consolidating federal loans into a Direct Consolidation Loan can open up repayment options and simplify your payments. But consolidation resets your progress toward forgiveness and may extend your repayment term. Do not consolidate without understanding those tradeoffs first.

Prepare now for the tax impact of forgiveness. If you are aiming for IDR forgiveness, start setting aside funds for the tax bill well before your forgiveness date. The IRS treats that forgiven amount as ordinary income, and a surprise five-figure tax bill the year of forgiveness is something you can plan around if you start early. You can read more about this in our guide to federal forgiveness programs.

Track deadlines and recertification dates. Income-driven plans require annual income recertification. Missing that deadline can result in a payment spike or removal from your plan. A system to track these dates, whether a calendar reminder or a document management service, is worth setting up from day one.

Stay informed on policy changes. Repayment options for students are changing faster than at any point in recent history. Bookmark reliable resources and check for updates regularly, especially if you are counting on forgiveness at a specific date.

Common pitfalls that derail repayment plans

Even borrowers who know their loan repayment schedule can run into costly surprises. Here are the most common traps and how to sidestep them.

Missing your first payment after the grace period ends. Federal loan default begins after 270 days of missed payments, but damage to your credit and servicer complications start much sooner. Set up autopay before your grace period ends, not after.

Assuming your current plan will stay the same. With SAVE, PAYE, and ICR phasing out by 2028, borrowers who do not actively select a plan risk being automatically transitioned to RAP or an amended IBR version that may not suit their situation.

Misunderstanding forgiveness eligibility. Not every repayment plan leads to the same forgiveness outcome. PSLF requires 10 years of qualifying payments on a specific plan while working for a qualifying employer. IDR forgiveness takes 20 to 30 years. Mixing up these paths leads to missed milestones.

Taking on additional loans without updating your repayment strategy. Borrowing additional federal loans after you have already started repayment can change your eligibility for certain plans and affect your servicer assignment.

Ignoring servicer errors. Servicers make mistakes. Payments can be misapplied, plan enrollments can lapse, and qualifying payment counts can be miscounted. Keeping your own records of every submission, payment, and communication is not optional. It is protection.

Staying organized is the most underrated part of managing a student debt repayment timeline. Borrowers who document everything have far more leverage when disputing errors or verifying forgiveness eligibility.

My take on repayment timelines right now

I have spent years watching borrowers approach their student loan repayment timeline in two ways. Some treat it as a fixed sentence to serve out. Others treat it as a financial variable they can influence. The second group almost always ends up better off.

What I have learned is that the biggest mistakes are not made in the numbers. They are made in the assumptions. Borrowers assume their plan will stay available. They assume forgiveness is guaranteed. They assume their servicer is tracking everything accurately. None of those assumptions are safe right now.

The 2026 changes are real, and the shift to RAP with its 30-year forgiveness window will catch a lot of people off guard. My honest take: if you have any flexibility in your budget, a faster repayment approach toward the standard plan saves you more money in total interest than any income-driven forgiveness strategy, especially now that forgiveness is taxable. The math only favors a longer timeline when your income is genuinely low relative to your debt.

Plan for the tax hit early. Keep your own records. Do not rely on your servicer to catch every error. And please, do not ignore a change letter from your servicer. Those letters often signal a plan transition that will affect your monthly payment. Every borrower I have seen get blindsided had one thing in common: they did not open the mail.

— Ellis

How TitanPrep can help you stay on track

Managing your student loan repayment timeline means keeping up with deadlines, plan changes, and paperwork that never seems to stop. TitanPrep is here to help you stay organized through every stage of that process.

Whether you need to understand the latest student loan policy updates, find the right repayment plan for your income, or lower your monthly payments before a payment increase hits, TitanPrep provides the document preparation and deadline tracking support you need. The client portal keeps your files organized and your submissions on record, so nothing falls through the cracks. TitanPrep does not guarantee outcomes, but it does give you the tools to stay prepared and compliant. Reach out today and get clarity on where your repayment stands.

FAQ

When does federal student loan repayment start?

For most Direct Subsidized and Unsubsidized loans, repayment starts after a 6-month grace period following graduation, withdrawal, or dropping below half-time enrollment. Parent PLUS loans have no automatic grace period and begin repayment immediately unless deferment is requested.

How long does it take to repay student loans?

The standard federal repayment plan takes 10 years, but the average borrower takes about 20 years due to income-driven plans. The new RAP plan, launching July 1, 2026, extends the forgiveness timeline to 30 years for eligible borrowers.

What is the Repayment Assistance Plan (RAP)?

RAP is a new federal income-driven repayment plan that replaces SAVE, PAYE, and ICR for new borrowers starting July 1, 2026. Payments are calculated at 1 to 10% of total adjusted gross income, with a $10 monthly minimum and forgiveness after 30 years.

Is student loan forgiveness taxable?

IDR forgiveness for loans forgiven after December 31, 2025, is treated as taxable income at the federal level. Public Service Loan Forgiveness remains tax-free under current law, which is a major distinction when comparing repayment strategies.

What happens if I do not choose a repayment plan?

You will be placed on the Standard Repayment Plan by default, or automatically transitioned to an available plan if your current plan is being phased out. Automatic transitions may result in higher payments or less favorable terms, so actively selecting your plan is always the better move.

Recommended

Comments