What Is Reconsideration for Loan Forgiveness?

- TitanPrep Official

- May 26

- 9 min read

Getting a denial on your loan forgiveness application is discouraging, but it is not necessarily the end of the road. Understanding what is reconsideration for loan forgiveness can make the difference between giving up and getting the outcome you deserve. Reconsideration is a formal process that lets you challenge a denial based on administrative errors or new evidence. It applies to specific federal programs, and knowing how to use it correctly gives you a real path forward. This guide walks you through everything you need to know.

Table of Contents

Key Takeaways

Point | Details |

Reconsideration fixes errors | The process corrects administrative mistakes like miscounted payments, not program rule changes. |

Two main programs apply | PSLF and Borrower Defense to Repayment are the primary programs with reconsideration options. |

Documentation is critical | Gathering employer certifications, payment records, and correspondence before filing strengthens your case. |

Expect significant wait times | Processing can take six months to over a year due to current Department of Education backlogs. |

Reconsideration vs. Buyback are different | PSLF Buyback requires a lump-sum payment; reconsideration is a free error-correction process. |

What reconsideration for loan forgiveness actually means

Loan forgiveness reconsideration is a formal process for challenging denied PSLF or Borrower Defense applications based on administrative errors. That distinction matters enormously. Reconsideration is not a general appeals system where you can argue that the rules should apply differently to your situation. It is specifically designed to correct factual mistakes made during the review of your original application.

The programs where reconsideration is available include Public Service Loan Forgiveness (PSLF) and Borrower Defense to Repayment (BDTR). Both are federal student loan programs administered by the U.S. Department of Education. Private loans are not eligible for either program, which means reconsideration does not apply to them at all.

Common reasons borrowers pursue reconsideration include:

Payments that were counted incorrectly or excluded from the total

Employer certifications that were rejected despite the employer qualifying

Processing errors during an income-driven repayment (IDR) recalculation

Documentation that was submitted but not properly reviewed

Administrative miscategorization of loan types or repayment periods

Reconsideration cannot make ineligible employment or payments qualify. If your job genuinely does not meet PSLF criteria or your payments were made under a non-qualifying plan, reconsideration will not change that. It corrects errors. It does not bend rules. Understanding that boundary upfront saves you time and frustration.

It also helps to know that reconsideration is distinct from processes like PSLF Buyback, which we will cover in detail later. They look similar on the surface but serve very different purposes.

Pro Tip: Before filing any reconsideration request, review your denial letter carefully. The letter should specify exactly why your application was denied, and that reason tells you whether reconsideration is the right tool or whether a different path makes more sense.

How to request reconsideration for loan forgiveness

The process for submitting a reconsideration request depends on which program denied your application. Here is a step-by-step breakdown of how it typically works.

Log in to StudentAid.gov. For PSLF, you will use the PSLF Help Tool to initiate a reconsideration request. For BDTR, you will access your case-specific file through the borrower defense portal. Borrowers must submit relevant documentation and respond in a timely manner to avoid request expiration.

Gather your documentation. Before you submit anything, collect every relevant document. This includes employer certification forms (ECF), your complete payment history from your servicer, tax returns, W-2s, and any correspondence related to your application or denial.

Write a clear statement of error. Your reconsideration request needs to explain specifically what you believe was processed incorrectly and why. Vague complaints do not move the needle. Point to specific payments, dates, employers, or documents that contradict the denial.

Submit supporting evidence. Attach every document that directly supports your claim. If you are disputing a miscounted payment, attach the proof of payment. If you are challenging an employer rejection, attach evidence of the employer’s qualifying status such as a 501©(3) determination letter or government agency verification.

File a Privacy Act request if needed. If you want to review your complete case file before or during the reconsideration process, you can submit a Privacy Act request to the Department of Education. Seeing your full file can reveal errors you were not aware of, including documentation that was lost or misfiled.

Track your submission and note the date. Keep a copy of everything you submit and record the date. This becomes your reference point if you need to follow up later.

Pro Tip: Request your complete loan payment history from your servicer before filing. Many miscounted payment disputes are resolved simply by presenting a detailed payment record alongside the reconsideration request.

You can also find detailed guidance through TitanPrep’s loan forgiveness application guide to help you prepare your documents correctly before submitting.

Common challenges and realistic timelines

Patience is one of the most important things you can bring to the reconsideration process. The Department of Education faces significant backlogs right now. Over 530,000 IDR applications are pending as of April 2026, and that volume directly affects how quickly reconsideration cases move.

Typical wait times for reconsideration range from six months to well over a year. Manual review is the standard, and that takes time even when your case is straightforward. Most borrowers describe a period of waiting with very little feedback, which understandably creates anxiety.

Here is how to manage the process while you wait:

Follow up at the six-month mark. Borrowers are advised to escalate reconsideration requests after six months of no updates because files can stall in manual processing queues. Contact your servicer and the Department of Education directly.

Document every communication. Write down dates, representative names, and the content of every call or email. If you need to escalate, this record supports your case.

Avoid common filing mistakes. Missing documents, unclear narratives, and misaddressed submissions are the top reasons reconsideration cases get denied again or stalled. Double-check your submission before sending.

Pursue parallel options. Reconsideration does not prevent you from exploring other paths at the same time. If you qualify, you can work toward switching repayment plans, applying for PSLF Buyback, or pursuing an ombudsman referral simultaneously.

“Reconsideration is not a passive process. Borrowers who stay organized, follow up consistently, and document everything are in a far better position than those who submit and wait quietly.”

Be honest with yourself about one other thing. Reconsideration cannot override statutory eligibility requirements. If you review your denial and realize your employer never qualified or your payments were made under a non-qualifying plan throughout, that is not an error to be corrected. It is a genuine eligibility issue that requires a different solution.

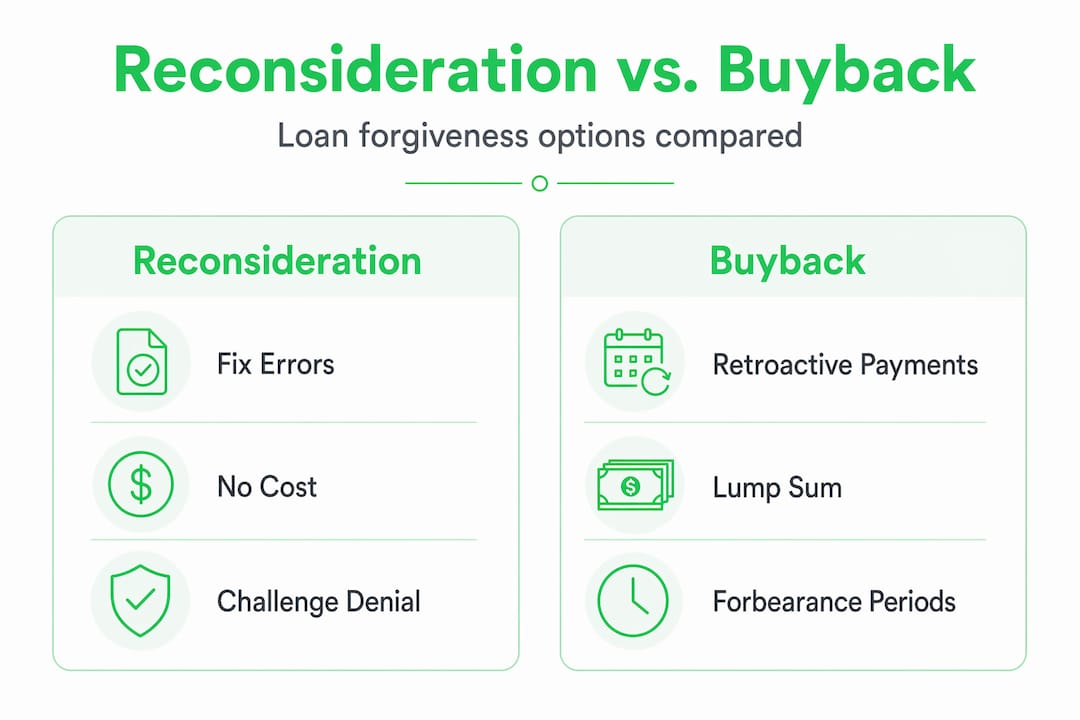

PSLF reconsideration vs. PSLF Buyback

These two options confuse a lot of borrowers, and the confusion makes sense. Both relate to PSLF, both address situations where qualifying time was not counted, and both are options you may consider after a denial. But they are fundamentally different processes.

Feature | PSLF Reconsideration | PSLF Buyback |

Purpose | Correct administrative errors in your application | Retroactively count deferment or forbearance months |

Cost to borrower | Free | Requires a lump-sum payment |

What it fixes | Miscounted payments, rejected employer certifications | Periods when you were in non-qualifying status |

Eligibility | Must have qualifying employment and loan type | Must have met all PSLF requirements except the ineligible period |

Outcome if approved | Corrected payment count, potential forgiveness | Months bought back, potential forgiveness |

PSLF Buyback allows borrowers to pay lump sums to retroactively count certain deferment or forbearance periods toward forgiveness. It differs significantly because it requires a financial payment and addresses non-qualifying periods, while reconsideration corrects errors at no cost.

If you were placed in forbearance under the SAVE plan and lost qualifying months as a result, Buyback may apply to you. Borrowers stuck in SAVE plan forbearance should consider pursuing PSLF Buyback while simultaneously switching to a qualifying repayment plan such as IBR, PAYE, or ICR. That parallel approach keeps progress moving even when the administrative process is slow.

The key question to ask yourself is this: was my denial caused by an error in how my application was reviewed, or by a period when I genuinely was not in a qualifying status? If it is an error, pursue reconsideration. If it is a non-qualifying period, look into Buyback. If you are unsure, Titanprep’s resource on PSLF automatic forgiveness can help you understand where your case might fit.

Building a strong Borrower Defense reconsideration case

Borrower Defense to Repayment reconsideration has stricter requirements than PSLF reconsideration. Simply restating your original claims or pushing back on how the rules were interpreted is not enough.

BDTR reconsideration requires new, concrete evidence that was not included in your original application. The Department of Education reviews these cases under 2016 regulations, which means the legal standard is specific. You need to show that the school made a misrepresentation and that you relied on that misrepresentation when making your enrollment decision.

When building your reconsideration case for BDTR, focus on these evidence types:

Enrollment materials and promotional content. Brochures, emails, website screenshots, or presentations that contained false claims about job placement rates, accreditation, or program outcomes.

Correspondence with school staff. Any written communication where staff made claims about your program that turned out to be false or misleading.

Affidavits from classmates or instructors. Witness statements from others who experienced the same misrepresentations can add significant weight to your case.

Official records of school violations. Regulatory findings, accreditation actions, or court documents that establish the school engaged in misconduct.

If your denial letter cited specific deficiencies, address each one directly and methodically. Do not submit a general narrative and hope for the best. Match your evidence to each point in the denial.

Pro Tip: If you have new allegations to add that were not part of your original BDTR application, those must be submitted as a separate application. Reconsideration only covers what was already reviewed.

You can also explore TitanPrep’s guidance on disputing unqualified loan debt if you believe your situation involves broader eligibility issues beyond the original application.

My honest take on the reconsideration process

I have seen borrowers go into reconsideration with high hopes and come out frustrated, not because the system failed them, but because they misunderstood what reconsideration can actually do. The most common misconception I encounter is that reconsideration is a second chance to qualify for forgiveness. It is not. It is a second chance to correct mistakes in your reviewed application.

In my experience, the borrowers who succeed in reconsideration are the ones who arrive with organized, specific documentation and a clear explanation of the error. Vague appeals rarely go anywhere. A three-page narrative about how unfair the process is will not move your file. A one-page statement identifying a specific miscounted payment with attached proof will.

The uncomfortable truth is that some denials are not errors. Some borrowers genuinely did not meet the criteria. If that is your situation, pushing reconsideration harder will not change the outcome. What it will do is delay you from finding the right solution, whether that is Buyback, switching repayment plans, or reconsidering your long-term strategy entirely.

What I recommend is this: be honest with yourself early. Review your denial. Ask whether the problem is a factual mistake or a genuine eligibility issue. Then act accordingly. The system is slow, yes. But borrowers who stay organized, communicate proactively with their servicers, and keep records of everything are the ones who stay on track regardless of the pace.

— Ellis

How TitanPrep can support your reconsideration efforts

Reconsideration cases are won and lost on documentation. Whether you are pursuing PSLF reconsideration or a Borrower Defense appeal, having your records organized and your submissions prepared correctly is what moves things forward.

TitanPrep helps borrowers organize, prepare, and track the paperwork involved in federal loan forgiveness programs, including PSLF and BDTR applications. Through TitanPrep’s client portal, you can upload documents, monitor your file status, and keep track of deadlines without worrying about things slipping through the cracks.

With student loan payments potentially tripling in 2025, staying on top of your forgiveness options has never mattered more. Titanprep also provides access to important loan forgiveness updates so you always know where programs stand. TitanPrep does not guarantee forgiveness outcomes. Eligibility is determined solely by the Department of Education or your loan servicer.

FAQ

What is reconsideration for loan forgiveness?

Reconsideration is a formal process that allows borrowers to challenge a denied PSLF or Borrower Defense application when the denial was based on an administrative error. It does not change program rules but corrects factual or processing mistakes in how the original application was reviewed.

How long does reconsideration take?

Wait times typically range from six months to over a year due to current administrative backlogs at the Department of Education. Borrowers should follow up after six months if they have not received any updates on their case.

Can reconsideration help if my employer never qualified for PSLF?

No. Reconsideration corrects errors in how your application was processed. If your employer genuinely did not meet PSLF eligibility criteria, reconsideration cannot override that statutory requirement.

What is the difference between PSLF reconsideration and PSLF Buyback?

PSLF reconsideration is a free process that fixes errors in your application, such as miscounted payments. PSLF Buyback requires a lump-sum payment and retroactively counts periods of deferment or forbearance that were not originally qualifying.

What new evidence do I need for a Borrower Defense reconsideration?

BDTR reconsideration requires new concrete evidence not included in your original application, such as enrollment materials with false claims, school correspondence, or regulatory records of misconduct. Simply restating your original claims is not sufficient for approval.

Recommended