The Role of Servicers in Student Loans Explained

- TitanPrep Official

- 4 days ago

- 9 min read

Most borrowers know they have student loans. Far fewer know who actually manages them. The role of servicers in student loans is one of the most misunderstood parts of the entire repayment process, and that confusion has real consequences. Miss a notice from your servicer, fail to re-enroll in auto-pay after a transfer, or overlook a repayment plan change, and you could end up with a damaged credit score or unnecessary interest charges. Understanding what servicers do, and how to work with them effectively, puts you in control of your own financial future.

Table of Contents

Key takeaways

Point | Details |

Servicers are not lenders | Your servicer manages your loan day-to-day but does not own it — the Department of Education does for federal loans. |

You cannot choose your servicer | The Department of Education assigns federal loan servicers; you find yours on StudentAid.gov. |

Transfers happen without warning | Servicer transfers require only 15-day notice and demand prompt action to protect your repayment status. |

Oversight gaps create real risk | Four out of five servicers failed accuracy metrics before 2025, which means verifying your own records matters. |

Documentation protects you | Keeping written records of every servicer interaction is your best defense against billing errors and disputes. |

The role of servicers in student loans

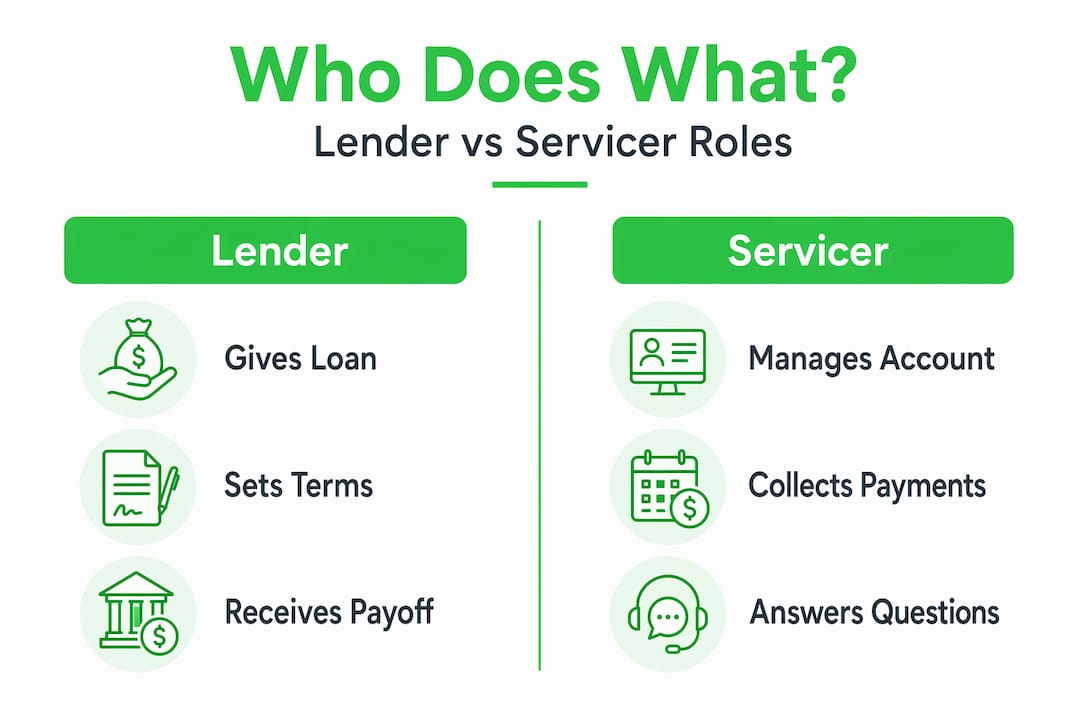

Before you can work the system effectively, you need to understand who you are actually dealing with. A loan servicer is not your lender. The servicer is an administrative intermediary. Think of the U.S. Department of Education as the owner of your federal loan and the servicer as the company hired to handle all day-to-day operations on that loan.

Borrowers and servicers are often confused for lenders, but the two roles are fundamentally different. The lender or loan owner holds the financial stake. The servicer handles billing, communication, repayment plan enrollment, and paperwork. You pay your servicer, not the Department of Education directly.

For federal loans, the Department of Education assigns your servicer. You do not get to choose. Your assigned servicer appears on your StudentAid.gov dashboard, and it is possible that a student borrower and a parent borrower on the same household have completely different servicers.

Private loan servicers operate differently. Private lenders sometimes service their own loans, or they contract with third-party servicers. The rules, protections, and repayment options for private loans vary widely because federal consumer protections do not apply in the same way.

Here is what distinguishes federal from private servicers at a glance:

Federal servicers are assigned by the Department of Education under contract and must follow federal rules on repayment options, deferment, and forbearance.

Private servicers operate under the terms of your private loan agreement, which means fewer standardized options and less regulatory protection.

Parent PLUS loan borrowers may have a different servicer than the student whose education the loan funded.

Multiple loans from different periods may be assigned to different servicers, which is why checking your StudentAid.gov dashboard regularly matters.

What servicers actually do every day

The student loan servicing process covers a lot more ground than most borrowers realize. Servicers are responsible for the full lifecycle of your loan from the day repayment begins until the day your balance reaches zero. Here is a breakdown of their core responsibilities:

Processing payments: Every payment you make goes through your servicer. They apply it to your balance according to federal rules (interest first, then principal, unless you direct otherwise).

Sending billing statements: Servicers issue monthly statements and payment due notices. These may arrive by email or mail depending on your preferences.

Managing repayment plan enrollment: If you want to switch from a standard plan to an income-driven repayment plan, you work directly with your servicer to change your repayment plan. They verify your income documentation and update your account.

Handling deferment and forbearance: If you lose your job or face financial hardship, your servicer processes deferment and forbearance requests. They are your first call when you need temporary relief from payments.

Administering forgiveness paperwork: Servicers manage forgiveness program documentation, including Public Service Loan Forgiveness (PSLF) employment certification forms and income recertification for IDR plans.

Maintaining loan records: Servicers maintain your loan records, including payment history, balance, and repayment plan status. These records feed into your credit report.

Reporting to credit bureaus: Your servicer reports your payment status monthly to the major credit bureaus. On-time payments build credit. Late or missed payments damage it.

Notifying you of account changes: When anything changes on your account, from interest rate adjustments to servicer transfers, the servicer must notify you in writing.

Pro Tip: Set your account preferences to receive both email and paper notices from your servicer. That way, if one delivery method fails, you still get critical updates about your loan.

What happens during a servicer transfer

Servicer transfers catch borrowers off guard more than almost any other event in the repayment process. The Department of Education controls which servicer manages your loans under its Next Gen servicing framework. At any point, they can reassign your loan to a different company, and you have limited recourse.

What the transfer does NOT do: it does not change your loan terms, your interest rate, your balance, or your repayment plan. Your debt remains exactly the same. What changes is who you send payments to and where you log in to manage your account.

Here is what to do when a transfer happens:

Watch for written notices. Transfers require 15-day advance written notice from both the outgoing and incoming servicers. Check your email and mail regularly in the weeks surrounding a known transfer date.

Create your new account. The incoming servicer will send you credentials or instructions to set up your new online account. Do this immediately. Waiting creates gaps in your ability to make payments or check your status.

Re-enroll in auto-pay. Auto-pay does not transfer automatically. If you were receiving a 0.25% interest rate reduction for auto-pay, you must re-enroll with the new servicer to keep that benefit.

Verify your payment history. Log in to your new account and confirm that your full payment history has transferred correctly. Errors happen, and catching them early is far easier than disputing records months later.

Confirm your repayment plan. Check that your income-driven repayment plan, deferment, or forbearance status transferred accurately. Verifying your loan data after a transfer is one of the most overlooked steps borrowers take too casually.

Stop using the old portal. Your old servicer’s website will no longer reflect your current account. Using it to check balances or make payments after the transfer date is a common mistake that leads to missed payments.

Pro Tip: Screenshot your current payment history, repayment plan status, and account balance before a known transfer date. That record is your evidence if the new servicer’s data does not match.

Transfer step | Why it matters |

Watch for written notice | You have only 15 days advance warning before the switch takes effect |

Set up new account promptly | Delays can interrupt payment access and create late payment risk |

Re-enroll in auto-pay | The interest rate discount does not carry over automatically |

Verify payment history | Errors in transferred records can affect credit and forgiveness counts |

Confirm repayment plan status | IDR and PSLF progress must be accurately reflected in the new system |

Servicer oversight and why it matters to you

Here is something most borrowers do not know: the quality of your servicer’s work is supposed to be regulated. The Federal Student Aid (FSA) office sets performance standards for accuracy and call quality as part of servicer contracts signed in April 2024. Servicers face financial penalties for failing to meet those standards.

The reality, though, is sobering. Four out of five servicers failed accuracy metrics before 2025. FSA paused strict oversight enforcement due to staff capacity issues. The Government Accountability Office (GAO) has since recommended that FSA resume full monitoring and apply penalties consistently.

“GAO recommends that FSA resume servicer oversight and enforce performance standards with financial penalties to protect borrowers from errors in billing and repayment status.” — GAO report on federal student loan servicer oversight

What does this mean for you in practical terms? Inaccurate servicer records can cause you to receive incorrect bills, have your repayment plan miscategorized, or lose credit toward forgiveness programs. These are not hypothetical risks. They have happened to real borrowers.

The best defense is active engagement. When you call your servicer, ask specific questions. Request confirmation of your repayment plan name, effective date, and next recertification deadline. Document the date, time, and representative name for every call. If you get incorrect information verbally, follow up with a written request by email or through the servicer portal. That paper trail can resolve disputes that would otherwise take months to untangle. You can read more about common servicer complaints that have escalated into legal action when borrowers lacked proper documentation.

How to manage your servicer relationship effectively

Knowing what servicers do is only half the equation. Knowing how to work with them is where most borrowers either succeed or fall behind. Here are the practices that make a real difference:

Find your servicer right now. Log in to StudentAid.gov and look under your loan details. Your servicer is listed there along with contact information. If you have multiple loans, you may have multiple servicers.

Keep your contact information current. Your servicer cannot reach you if your phone number, email, or address is outdated. Update your information every time something changes. Critical notices, including transfer alerts and recertification reminders, are sent to the contact information on file.

Use the online portal and auto-pay. Making payments through your servicer’s online portal reduces the chance of processing errors. Auto-pay also gets you a 0.25% interest rate reduction on most federal loans, which adds up over time.

Check your account monthly. Do not wait for a problem to check in. Review your balance, payment application, and plan status every month. Servicers are the front door to account updates, plan changes, and payment documentation, and errors are easier to catch when you are paying attention.

Know how to escalate a complaint. If your servicer gives you incorrect information or fails to correct an error, you can file a complaint with the FSA Ombudsman or submit a complaint through the Consumer Financial Protection Bureau (CFPB). If you are dealing with a specific servicer issue, resources like Aidvantage complaint guidance can show you exactly what to document and how to escalate.

Watch for loan scams. Scammers sometimes send communications that mimic servicer notices, complete with logos and official-sounding language. Always verify by logging directly into your servicer’s official site rather than clicking links in unsolicited emails or texts.

Pro Tip: Asking clarifying questions during servicer calls, such as “Can you confirm my current repayment plan and when it was last updated?”, is one of the most effective ways to catch errors before they cause real damage.

My take on servicer relationships

I’ve worked with student loan borrowers long enough to see the same pattern repeat itself. Borrowers treat their servicer like a billing company and nothing more. They make their payment, close the portal, and move on. Then something goes wrong, and they have no records, no notes, and no idea when their repayment plan was last updated.

What I’ve learned is that servicers are not adversaries. They are also not infallible. The GAO data on accuracy failures tells you everything you need to know: the system is imperfect, and passive borrowers absorb the cost of that imperfection.

My honest advice is to treat your servicer account the way you would treat a bank account. Check it regularly, document everything, and never assume that information you received six months ago is still accurate. The borrowers I’ve seen avoid the most serious problems are the ones who stay engaged, ask specific questions, and keep written records of every interaction. That is not paranoia. That is just good financial management applied to a very large debt.

— Ellis

How TitanPrep helps you stay organized

Knowing the role servicers play is the first step. Staying on top of deadlines, documents, and repayment plan requirements is where many borrowers need real support. TitanPrep specializes in helping federal student loan borrowers organize and submit paperwork for programs like IDR, PSLF, and discharge options. Through TitanPrep’s client portal, you can upload documents, track submission status, and maintain records of your communications with servicers.

If you are not sure where to start, the TitanPrep how it works page walks you through the full support process. For answers to the most common questions about repayment programs and servicer interactions, the student loan FAQ is a solid resource to bookmark. TitanPrep does not guarantee specific outcomes. Eligibility for any federal program is determined by the Department of Education or your loan servicer.

FAQ

What does a student loan servicer do?

A student loan servicer manages all day-to-day operations on your loan, including billing, payment processing, repayment plan enrollment, and deferment or forbearance requests. They also maintain your loan records and report your payment history to credit bureaus.

Can I choose my federal student loan servicer?

No. The U.S. Department of Education assigns your federal loan servicer, and you cannot change that assignment. You can find your assigned servicer by logging in to your StudentAid.gov account.

What should I do when my servicer changes?

When a servicer transfer happens, you should set up your new account immediately, re-enroll in auto-pay to retain your interest rate discount, and verify that your payment history and repayment plan transferred correctly to the new servicer.

Why does servicer accuracy matter for my loans?

Inaccurate servicer records can lead to incorrect billing, misapplied payments, and lost progress toward forgiveness programs. GAO reports that a majority of servicers failed accuracy metrics before 2025, which makes personal record-keeping critical for all borrowers.

How do I file a complaint against my servicer?

You can file a complaint with the FSA Ombudsman or submit one through the Consumer Financial Protection Bureau (CFPB). Before escalating, document the specific error, the date you reported it, and any written or verbal responses you received from the servicer.

Recommended

Comments