Loan Forgiveness Application Process: 2026 Guide

- TitanPrep Official

- 2 days ago

- 8 min read

Applying for federal student loan forgiveness sounds straightforward until you are deep in paperwork, unsure which forms to submit, and watching deadlines pass. The loan forgiveness application process trips up even organized borrowers because the rules are specific, the timelines are long, and one missed step can reset your progress. This guide walks you through eligibility, the actual application steps for major federal programs, common mistakes to avoid, and what to expect from a tax perspective so you can move forward with confidence rather than confusion.

Table of Contents

Key takeaways

Point | Details |

Verify loan type first | Only Direct Loans qualify for PSLF and most IDR forgiveness without consolidation. |

Repayment plan selection matters | Choosing the wrong plan at the start can disqualify payments already made. |

Annual certification protects you | Submitting your Employment Certification Form every year keeps your payment count accurate. |

PSLF forgiveness is tax-free | IDR forgiveness after 20 to 25 years is generally taxable starting in 2026. |

Denials are not final | The PSLF Reconsideration process allows you to challenge errors in employer verification or payment counts. |

Understanding your eligibility before applying

Before you touch a single application form, you need to know whether your loans and repayment plan actually qualify. This step is where most borrowers lose time.

Qualifying loan types

Direct Loans are the primary loan type accepted for both Public Service Loan Forgiveness and income-driven repayment forgiveness. If you have older Federal Family Education Loan (FFEL) or Perkins loans, they do not automatically qualify. You would need to consolidate them into a Direct Consolidation Loan first. That consolidation step adds time, so plan for it early.

Pro Tip: Consolidating FFEL or Perkins loans into a Direct Consolidation Loan resets your payment count. If you have already made qualifying payments, consolidate only when the benefits clearly outweigh the cost.

Repayment plans that count

Not every repayment plan counts toward forgiveness. The plans that do include:

Income-Based Repayment (IBR)

Pay As You Earn (PAYE)

Income-Contingent Repayment (ICR)

The new Repayment Assistance Plan (RAP)

Standard 10-Year Repayment (for PSLF only)

As of May 2026, RAP payments count toward PSLF if all other criteria are met. That is a significant update worth noting if you recently switched plans.

PSLF employment eligibility

For PSLF specifically, you must work full-time for a qualifying employer. That means a government agency at any level, a 501©(3) nonprofit, or certain other public service organizations. You can confirm whether your employer qualifies using the PSLF Help Tool at StudentAid.gov before you commit to the program.

PSLF requires 120 qualifying payments while working full-time for an eligible employer. You also need to submit the Employment Certification Form annually, not just at the end of 10 years. Annual submission keeps your payment count current and flags any errors early. You can learn more about staying PSLF compliant in TitanPrep’s dedicated PSLF guide.

For IDR forgiveness, you do not need a specific employer. You do need to select the correct repayment plan upfront, recertify your income annually, and stay enrolled consistently. The forgiveness clock runs for 20 to 25 years depending on your plan. RAP extends that to 30 years.

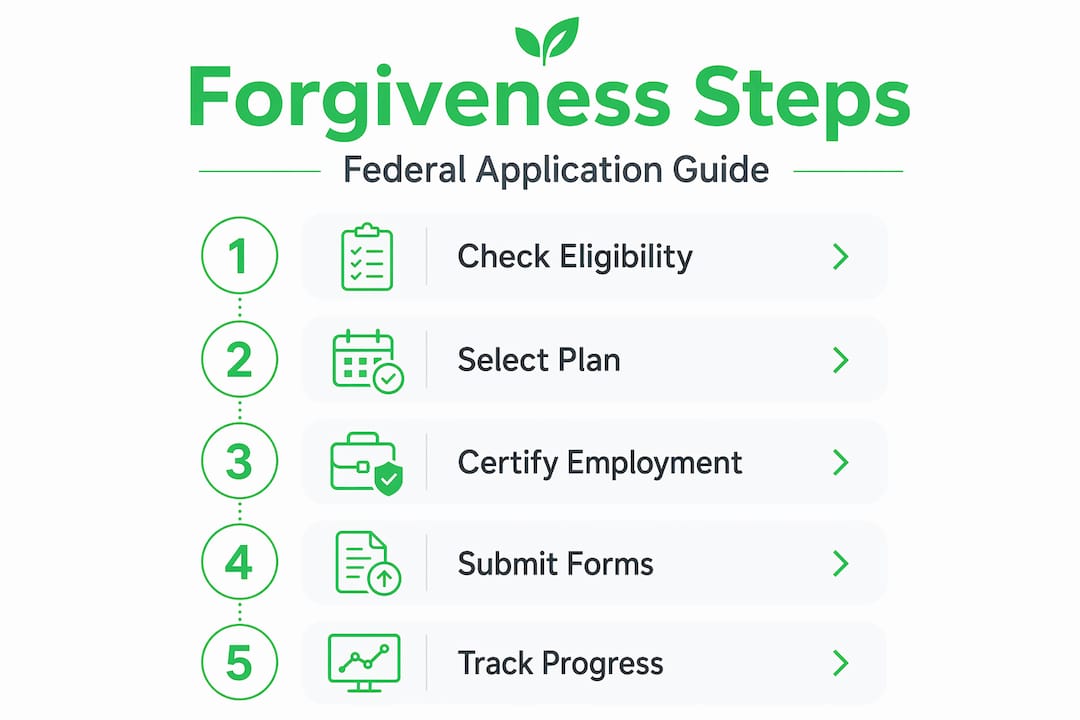

Step-by-step application process for federal programs

The actual application steps differ slightly depending on whether you are pursuing PSLF or IDR forgiveness. Here is how each process works.

For PSLF applicants

Log in to StudentAid.gov and use the PSLF Help Tool to verify your employer and loan types.

Consolidate if needed. If you have FFEL or Perkins loans, submit a Direct Consolidation Loan application first and then enroll in a qualifying repayment plan.

Submit the Employment Certification Form (ECF) annually. This is technically called the PSLF Form. Your employer must sign it each year.

Check your payment count after each ECF submission. Your servicer will send a letter confirming your count. If it looks wrong, contact your servicer right away.

Submit the final PSLF application once you reach 120 qualifying payments. You do this through StudentAid.gov as well.

Respond to any action requests. If your application goes to an “Action Required” status, respond promptly. Ignoring it can extend your wait significantly.

Pro Tip: Do not wait until you hit 120 payments to submit your first ECF. Borrowers who certify employment from year one are far less likely to face disputes over payment counts later.

For IDR forgiveness applicants

Step | Action | Where to complete |

1. Enroll in IDR plan | Choose IBR, PAYE, ICR, or RAP | |

2. Annual recertification | Recertify income and family size every 12 months | StudentAid.gov or servicer |

3. Track payment count | Monitor your IDR payment tracker | Loan servicer account |

4. Apply for forgiveness | Submit forgiveness request after qualifying period | Servicer-specific process |

5. Report to IRS | Report forgiven amount as income (post-2026) | IRS Form 1099-C |

IDR forgiveness does not require a separate employer certification, but the recertification deadline is strict. Missing it can bump you off your plan temporarily and disrupt your payment count. A new streamlined rehabilitation and IDR enrollment process introduced in May 2026 makes it easier for borrowers in default to re-enter the system and resume progress.

Check the loan forgiveness requirements outlined by TitanPrep to make sure you have the right plan matched to your situation.

Common issues, mistakes, and how to appeal

Even borrowers who follow every step carefully sometimes run into problems. Knowing what to expect helps you resolve issues without losing months of progress.

The most frequent reasons applications stall or get denied include:

Employer verification errors. If your employer’s name on file does not match official records, your certification can be rejected.

Payment discrepancies. Payments made under a non-qualifying plan or during a deferment period do not count. Your payment history needs to match program requirements exactly.

Incorrect loan type. Submitting a PSLF application with unconsolidated FFEL loans is a common error.

Missed recertification deadlines. This affects IDR borrowers more often than PSLF borrowers and can cause plan disruptions.

Non-responsive employers. If your current or former employer will not sign the ECF, that delays your entire certification.

Pro Tip: If your employer has closed or is unresponsive, contact your loan servicer directly and explain the situation. There are processes in place for exactly this scenario, including using alternative documentation.

What to do after a denial

A denial is not the end of the road. PSLF denials can often be reversed through the formal Reconsideration process, which allows you to submit supporting documentation to challenge errors. Start by requesting a detailed explanation of why your application was denied. From there, gather records like pay stubs, employer tax documents, or correspondence to support your case.

PSLF applications typically take 2 to 6 months to process. If you are deep in that window and see an “Action Required” flag, treat it as urgent. Delays caused by slow responses from the borrower are the most preventable kind.

Tracking your payments manually through the IDR payment tracker and keeping copies of every submitted form gives you evidence to dispute errors quickly. TitanPrep’s resources on education department guidance can help you stay current on regulatory changes that affect your case.

Tax implications of loan forgiveness in 2026

This is the part many borrowers overlook until the bill arrives. The tax treatment of your forgiven balance depends entirely on which program discharged it.

PSLF forgiveness is permanently excluded from federal taxable income. You will not owe the IRS anything on the forgiven balance. That is not true for IDR forgiveness.

Starting in 2026, IDR forgiveness is generally taxable as cancellation of debt income. That means if $40,000 of your loans are forgiven through IBR after 25 years, you may owe income tax on that full amount in the year it is discharged. A Form 1099-C arrives in January or February for the prior calendar year in which debt was canceled, and you report it on your return.

Practical steps to prepare:

Estimate your forgiven balance and model the potential tax impact before your discharge year arrives.

Adjust your tax withholdings or make estimated quarterly payments in the year your forgiveness is expected.

If your total debts exceed your total assets at the time of discharge, you may qualify for the insolvency exclusion. File IRS Form 982 to claim it.

Keep records of every loan statement, repayment history, and servicer communication for your tax preparer.

Borrowers relying on IDR forgiveness should plan for the tax year the discharge is recognized and set aside funds or adjust withholdings accordingly. Getting surprised by a large tax bill after years of careful repayment is avoidable with early planning.

The distinction between PSLF and IDR tax treatment is one of the clearest reasons to evaluate which program genuinely fits your career and financial situation before you commit. If you are not sure which applies to you, the repayment options comparison at TitanPrep is a useful starting point.

My honest take on what actually trips borrowers up

I have spent years watching borrowers do everything right on paper and still lose progress because of small, avoidable oversights. The most common one? Treating the Employment Certification Form as a one-time task. Many borrowers submit it when they first enroll in PSLF and then forget about it for years. When they finally apply for forgiveness, they discover that several years of payments were never officially certified. Reconstructing that history is possible but slow.

The second thing I have seen consistently is borrowers choosing a repayment plan based on the lowest monthly payment without checking whether it qualifies for their target forgiveness program. The correct repayment plan selection is not a minor detail. It determines whether every payment you make counts at all.

I also want to be honest about processing times. Two to six months is the typical range, but I have seen cases take longer when documentation is incomplete or when borrowers do not respond quickly to servicer requests. Patience is necessary, but passive waiting is not. Check your application status regularly and respond the same day when action is requested.

Finally, do not let regulatory changes paralyze you. Programs like RAP are new, and some borrowers are waiting to see how the rules settle before applying. That caution is understandable, but every month you delay is a month that does not count toward forgiveness. Apply now based on what the current rules say, and adjust if needed.

— Ellis

How TitanPrep can help you stay on track

Preparing a loan forgiveness application takes more than filling out a form. It requires organized documentation, accurate payment records, and consistent follow-through across years or even decades of repayment. That is exactly where TitanPrep helps.

TitanPrep is a document preparation and support service for federal student loan borrowers. The team helps you organize and submit paperwork for programs like PSLF, IDR forgiveness, and certain discharge options. The client portal lets you upload documents, track deadlines, and monitor the status of your file in one place.

Get started by reviewing the top federal forgiveness programs TitanPrep has compiled, and explore the latest student loan updates to make sure you are working with current information. Note that applying for forgiveness through StudentAid.gov is free, and TitanPrep does not guarantee any outcome. Eligibility decisions are made solely by the U.S. Department of Education or your loan servicer.

FAQ

What is the loan forgiveness application process?

The loan forgiveness application process is the series of steps a borrower takes to verify eligibility, submit required forms, and receive discharge of their remaining federal student loan balance under programs like PSLF or IDR forgiveness. The process involves confirming loan types, selecting a qualifying repayment plan, certifying employment or income annually, and submitting a final application through StudentAid.gov or your loan servicer.

How long does the PSLF application take to process?

PSLF applications typically take 2 to 6 months to process after submission. Responding promptly to any servicer requests for additional documentation can prevent unnecessary delays.

Can a denied loan forgiveness application be appealed?

Yes. Borrowers denied PSLF can use the formal Reconsideration process to submit supporting documentation and challenge errors related to employer verification or payment counting. A denial should not be treated as a final decision without first reviewing the reason and gathering evidence.

Is forgiven student loan debt taxable?

It depends on the program. PSLF forgiveness is not taxable at the federal level. IDR forgiveness is generally taxable as cancellation of debt income starting in 2026, meaning you may owe income tax on the forgiven amount in the year it is discharged.

What loans qualify for federal loan forgiveness programs?

Direct Loans qualify for both PSLF and IDR forgiveness without additional steps. FFEL and Perkins loans must be consolidated into a Direct Consolidation Loan before they can qualify, which resets the payment count.

Recommended

Comments