The Role of Federal Government in Student Loans: 2026 Guide

- TitanPrep Official

- May 26

- 9 min read

The role of federal government in student loans has never been more complex, or more consequential, than it is right now. The federal government controls roughly $1.6 trillion in outstanding student loan debt, making it by far the largest provider of education financing in the country. For current borrowers, that means the rules set in Washington directly shape your monthly payments, your forgiveness eligibility, and even the consequences of missing a payment. With sweeping changes taking effect in 2026, understanding how the system works is no longer optional. It is the foundation of every smart borrowing and repayment decision you can make.

Table of Contents

Key Takeaways

Point | Details |

Federal government is primary lender | The U.S. government originates and backs the vast majority of student loans through Direct Loan programs. |

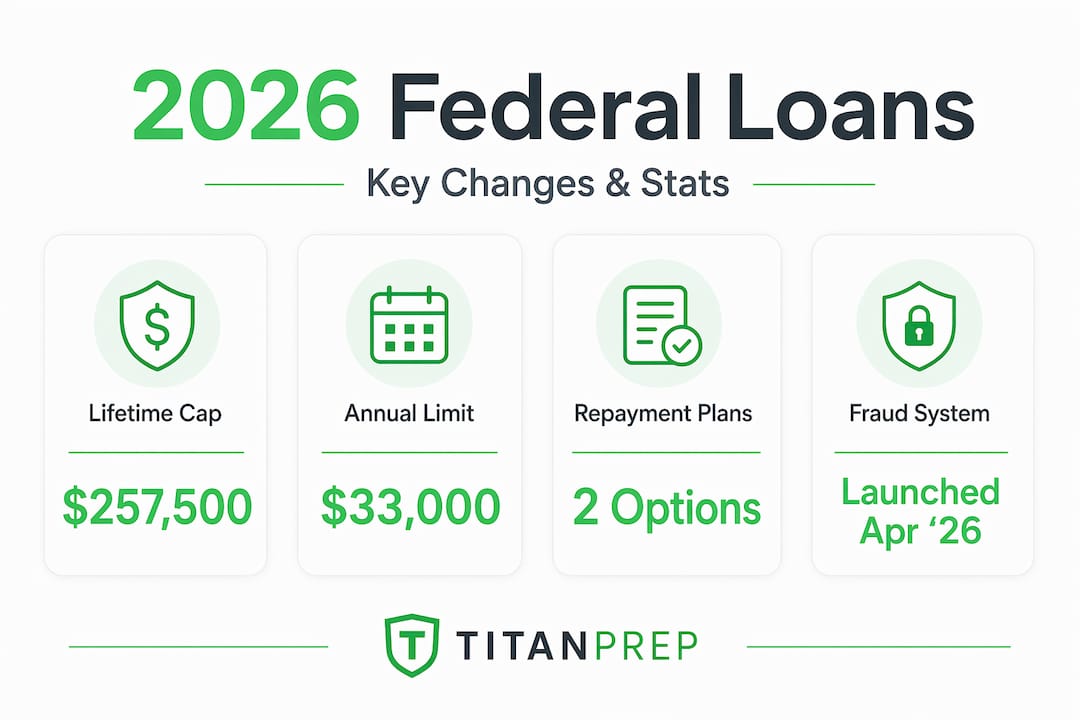

2026 borrowing caps are now in effect | A lifetime borrowing limit of $257,500 applies to most federal borrowers starting July 1, 2026. |

Repayment plans are being simplified | Legacy income-driven plans phase out by July 2028, replaced by two main options: Tiered Standard and RAP. |

Default collections moved to Treasury | The Department of Education partnered with Treasury in March 2026 to manage defaulted loan collections. |

Proactive action protects your options | Borrowers who review their plans now avoid being caught off guard as legacy programs close. |

How the federal government became the dominant student lender

The federal government did not always sit at the center of student loan financing. That role developed gradually, driven by a clear public interest goal: making higher education accessible to Americans regardless of income.

The foundation was laid with the Higher Education Act of 1965. That legislation created the first federal student loan programs under a model where the government guaranteed loans made by private banks. Known as Guaranteed Student Loans (GSL), these loans relied on private lenders but used federal backing to reduce lender risk. This arrangement worked for decades but proved expensive. Private lenders collected profits while taxpayers absorbed the defaults.

Congress restructured the system significantly in the 1990s and then decisively in 2010, when the Health Care and Education Reconciliation Act eliminated federally guaranteed private loans entirely. From that point forward, the Department of Education became the direct lender through what is now called the William D. Ford Federal Direct Loan Program. This shift had real consequences for borrowers. It centralized oversight, standardized terms, and removed private profit from the equation.

The core reasons the federal government plays this role are:

Access: Private lenders assess creditworthiness. Most 18-year-old students have none. Federal loans require no credit check for undergraduates, making college financing available to first-generation students and low-income families who would otherwise be locked out.

Affordability: Federal interest rates are set by Congress, not markets. This keeps rates predictable and often below what private lenders charge, especially for undergraduates.

Public interest: Higher education produces economic and civic benefits that extend beyond the individual borrower. Federal investment reflects that broader return.

Consumer protections: Federal loans come with built-in protections, including income-driven repayment, deferment, and forgiveness programs, that private loans generally do not offer.

State governments and private lenders still play roles in education financing, but neither approaches the scale or depth of federal involvement. Understanding this distinction helps you recognize why federal student loan policies carry so much weight in your financial life.

Current federal loan programs and 2026 changes

The federal loan portfolio covers several distinct programs, each with its own rules, limits, and eligibility requirements. The 2026 reforms made significant changes to these structures.

Here is a comparison of the key federal loan types and their current limits:

Loan Type | Who It’s For | 2026 Annual Limit | 2026 Aggregate Limit |

Direct Subsidized Loan | Undergraduates with financial need | Up to $5,500 (dependent) | $23,000 |

Direct Unsubsidized Loan | Undergraduates and graduates | Varies by year and status | $57,500 (undergrad) |

Graduate Direct Loan | Graduate students | $20,500 | Program aggregate caps apply |

Professional Degree Loan | Medical, law, and similar programs | $50,000 | Program aggregate caps apply |

Parent PLUS (revised) | Parents of undergrads | $20,000 | $65,000 total |

One of the most significant changes in 2026 is the establishment of a lifetime borrowing cap of $257,500, covering the full arc from undergraduate through doctoral-level study. This cap is new and applies to federal borrowing in total across a borrower’s lifetime. Equally significant, the Graduate PLUS loan program has been eliminated under 2026 rules, replaced by capped Direct Loan amounts for graduate and professional students.

On the integrity side, the Department of Education launched a real-time fraud detection system in April 2026 that is expected to save over $1 billion in the 2026-27 aid cycle. Applicants flagged by the system must verify their identity using government-issued credentials. This protects both the program and legitimate borrowers.

Pro Tip: If you are currently in graduate or professional school, check your cumulative federal borrowing now. Knowing exactly where you stand relative to the new caps helps you plan whether private loans may need to fill any gap before graduation.

The overhaul of federal repayment plans

Repayment used to mean choosing from a long list of options, including Standard, Extended, Graduated, Pay As You Earn (PAYE), Revised Pay As You Earn (SAVE), Income-Based Repayment (IBR), and Income-Contingent Repayment (ICR). That list is shrinking fast.

Under the 2026 reforms, the federal repayment system is consolidating to two primary plans:

Tiered Standard Repayment Plan: A structured plan with fixed payments calculated based on loan balance and income tier. This replaces the old standard and graduated plans. Payments are predictable and designed to fully pay off the loan within a set term.

Repayment Assistance Plan (RAP): The new income-sensitive option. RAP replaces SAVE, PAYE, and ICR. Critically, it is structured to prevent negative amortization, meaning the government subsidizes any unpaid interest so your balance never grows beyond what you borrowed.

The phaseout of legacy plans like SAVE, PAYE, and ICR will conclude by July 2028. If you are currently enrolled in one of these plans, you will eventually be transitioned. Acting before the deadline gives you more control over that process.

For Public Service Loan Forgiveness (PSLF) borrowers, qualifying payments made under RAP count toward the 120-payment threshold. The path to forgiveness remains open. But borrowers need to understand which plans qualify and confirm their employment certification is current. TitanPrep’s guidance on new forgiveness rules explains these updates in practical terms.

Pro Tip: Do not wait for your servicer to notify you about plan changes. Log into your studentaid.gov account today and review which repayment plan you are currently enrolled in. Transitions are easier when you initiate them rather than react to them.

The federal role in default management and collections

Default is where federal involvement becomes most consequential for borrowers in financial difficulty. The consequences are serious, and recent changes have shifted who manages them.

In March 2026, the Department of Education announced a historic partnership with Treasury to transition default loan collection functions to the Treasury Department. The goals are to reduce taxpayer costs and improve the rate at which defaulted borrowers return to active repayment.

Here is what happens when a federal loan goes into default, and what your options are:

Loan acceleration: Your full remaining balance becomes due immediately, not just missed payments.

Wage garnishment: The government can garnish up to 15% of disposable income without a court order.

Treasury offset: Tax refunds, Social Security benefits, and other federal payments can be withheld automatically.

Credit damage: Default is reported to credit bureaus, affecting your ability to borrow, rent housing, or in some cases, find employment.

Loss of federal aid eligibility: You cannot access new federal student loans or grants while in default.

The good news is that borrowers have options. The 2026 regulations allow borrowers who previously completed loan rehabilitation a second chance at rehabilitation. This is a meaningful change. Previously, rehabilitation was a one-time option. Extending access to a second round acknowledges that financial hardship is rarely a one-time event. Research also shows that default can deepen financial hardship for low-income borrowers, which makes early intervention critical.

Act quickly if you receive a default notice. Borrowers have a critical 30 to 65-day window after that notice to enter repayment or rehabilitation before harsher penalties activate.

Practical steps for borrowers in 2026

Knowing how the system works is useful. Knowing what to do with that knowledge is what protects you. Here are the most practical steps you can take right now:

Check your loan balance and borrowing history at studentaid.gov. This is especially urgent if you are still in school and approaching the new lifetime cap.

Review your current repayment plan and confirm whether it will still exist by July 2028. If you are on SAVE, PAYE, or ICR, start exploring how to change your repayment plan before your servicer makes that decision for you.

Recertify your income annually if you are on an income-driven plan. Missing the recertification deadline can push you off your plan and spike your monthly payment.

Confirm PSLF employment certification is up to date if you work in public service. Submit your Employment Certification Form every year, not just when you are close to 120 payments.

Contact your servicer immediately if you are behind on payments. Deferment and forbearance options still exist under 2026 rules, and entering them proactively is far better than defaulting.

Stay informed. Federal student loan policies are changing rapidly. Bookmark official sources and check for updates at least quarterly.

The 2026 reforms aim to limit overborrowing and curb tuition inflation by capping loan availability. That is a legitimate policy goal, but it places more responsibility on individual borrowers to plan carefully.

My take on where federal policy leaves borrowers right now

I have spent years working through the details of federal student loan policies, and my honest assessment of the 2026 reforms is mixed. The simplification of repayment into two plans is genuinely good for most borrowers. Choice paralysis is real. When people face eight repayment options, they often pick the default or nothing at all, which is rarely the right answer. Two clear options with predictable rules reduce that confusion.

What concerns me is the assumption embedded in the new borrowing caps. Caps on graduate borrowing may reduce debt loads for some students, but they will also push more borrowers toward private loans, which carry none of the federal protections. A borrower who cannot access enough federal funding and turns to a private lender has traded stability for access. That tradeoff is not always visible at the time of enrollment.

The Treasury transition for default collections is a sound administrative move, but it does not change the underlying reality: defaulting on a federal loan carries severe consequences that fall hardest on borrowers who were already struggling. The legal and regulatory changes around federal loan enforcement are worth reading carefully if you have any loans near delinquency.

My consistent advice is to treat your federal loans as an active financial obligation, not a deferred problem. The borrowers I have seen manage these programs well are the ones who check their accounts regularly, respond to servicer notices immediately, and ask for help before things escalate.

— Ellis

How TitanPrep helps you stay on track

Federal student loan policies are changing at a pace that makes it easy to fall behind. TitanPrep is a document preparation and support service that helps borrowers organize and submit paperwork for programs including Income-Driven Repayment, Public Service Loan Forgiveness, and borrower discharge options where applicable. The team tracks deadlines, stores records securely, and helps you maintain clear documentation of every submission and communication with your loan servicer.

If you want to understand exactly how the service works, visit TitanPrep’s How It Works page for a clear breakdown. For borrowers who need current updates on loan policy changes, the important loan updates page covers 2026 regulatory developments in plain language. TitanPrep does not guarantee outcomes. Eligibility decisions rest with the Department of Education and your servicer. But having your paperwork organized and submitted correctly is where every successful application begins.

FAQ

What is the federal government’s main role in student loans?

The federal government acts as the primary lender, regulator, and servicer for most student loans in the United States. Through the Direct Loan program, it originates loans, sets interest rates and terms, administers repayment plans, and manages forgiveness programs.

How much can I borrow in federal student loans over my lifetime?

Starting July 1, 2026, most borrowers face a lifetime federal borrowing cap of $257,500, covering undergraduate through doctoral-level education. Specific annual limits vary by student category and degree program.

What repayment plans will be available after 2028?

By July 2028, the federal repayment system will primarily offer two plans: the Tiered Standard Repayment Plan and the Repayment Assistance Plan (RAP). Legacy plans including SAVE, PAYE, and ICR are being phased out.

What happens if I default on a federal student loan?

Defaulting triggers loan acceleration, wage garnishment of up to 15% of disposable income, and Treasury offsets against tax refunds or federal benefits, all without a court order. Borrowers have a 30 to 65-day window after a default notice to enter rehabilitation or repayment to avoid the worst penalties.

Does RAP still qualify for Public Service Loan Forgiveness?

Yes. Payments made under the Repayment Assistance Plan count toward the 120-payment requirement for PSLF. Borrowers pursuing forgiveness should confirm their plan enrollment and employment certification are current with their loan servicer.

Recommended

Comments