Parent PLUS Loan Repayment Options: 2026 Guide

- TitanPrep Official

- 6 days ago

- 8 min read

If you borrowed a Parent PLUS loan to help your child through college, you may feel like your repayment options are limited. Many parents believe forgiveness is off the table and that they are stuck with whatever payment the loan servicer assigns them. That is not entirely true, but the window to access the best parent plus loan repayment options is closing faster than most families realize. New legislation is reshaping what is available, and a critical deadline in mid-2026 will permanently lock some borrowers out of more affordable plans.

Table of Contents

Key takeaways

Point | Details |

Consolidation is the gateway | You must consolidate into a Direct Consolidation Loan to access income-driven repayment plans. |

Act before June 30, 2026 | Your consolidation loan must be disbursed by this date to preserve IDR and forgiveness eligibility. |

New loans after July 1, 2026 | Borrowing any new Parent PLUS loan after this date removes IDR access for all your existing loans. |

PSLF is still possible | Parents can qualify for Public Service Loan Forgiveness after consolidation and enrollment in an eligible IDR plan. |

Refinancing has trade-offs | Private refinancing can lower your rate but permanently ends federal protections and forgiveness eligibility. |

Parent PLUS loan repayment options before consolidation

Before you consolidate, Parent PLUS loans offer three plans: Standard, Graduated, and Extended. None of them are income-based.

Standard Repayment spreads your balance over 10 years with fixed monthly payments. It is the default plan, and it means you pay the least in total interest. But the monthly payment on a $50,000 loan at 8.05% can exceed $600, which is a real strain for many families.

Graduated Repayment starts with lower payments that increase every two years. It still runs 10 years and costs more in total interest than Standard. This plan can work if you expect your income to grow but want breathing room early on.

Extended Repayment stretches payments out to 25 years. Your monthly amount drops significantly, but you pay substantially more interest over time. On a $50,000 loan, the difference in total interest between Standard and Extended can exceed $30,000.

Here is a quick comparison to put those differences in perspective:

Loan balance | Plan | Term | Est. monthly payment | Total interest paid |

$50,000 | Standard | 10 years | ~$610 | ~$23,200 |

$50,000 | Graduated | 10 years | ~$420 to $840 | ~$27,000 |

$50,000 | Extended | 25 years | ~$390 | ~$67,000 |

The key limitation across all three plans is the same. None of them offer income-based forgiveness. If you hit a rough financial stretch, your payment does not adjust. That is exactly why consolidation matters so much.

How consolidation unlocks income-driven repayment

Consolidation is a structural step, not a financial shortcut. It does not lower your interest rate or reduce your balance. What it does is convert your Parent PLUS loan into a Direct Consolidation Loan, which is a different loan type that qualifies for income-driven repayment (IDR) plans.

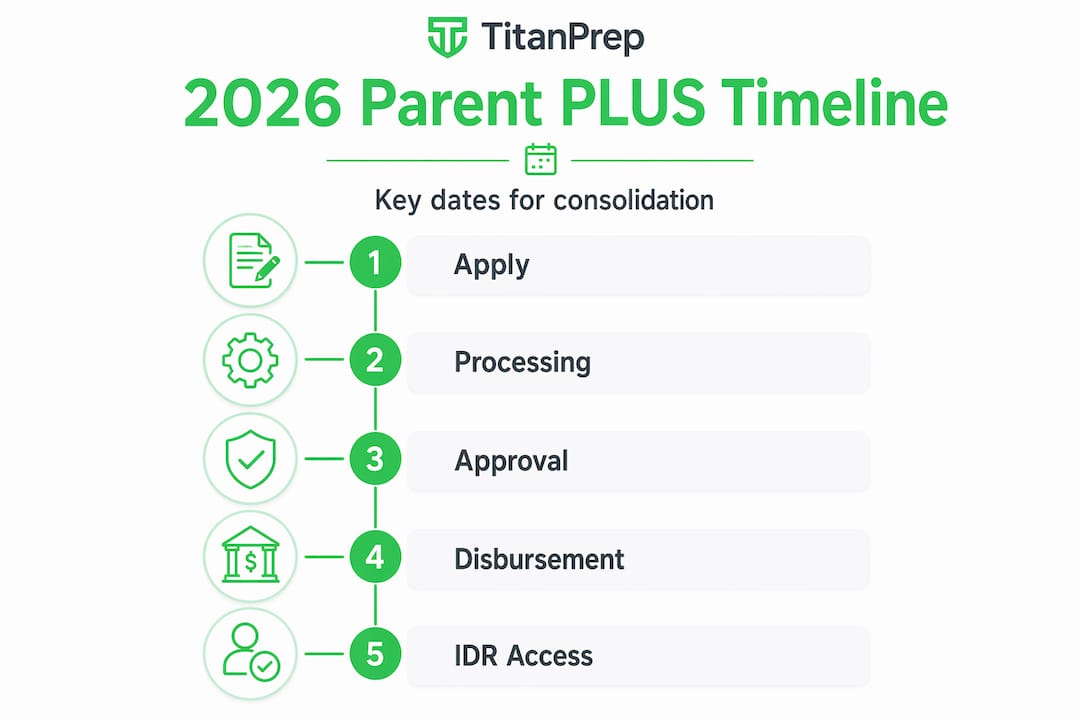

Here is the sequence you need to follow:

Apply for a Direct Consolidation Loan through studentaid.gov

Enroll in Income-Contingent Repayment (ICR) once the consolidation is complete

Make at least one qualifying payment under ICR

Switch to Income-Based Repayment (IBR), which typically offers lower payments

Why not stay on ICR? ICR is often not affordable long-term because it caps payments at 20% of your discretionary income, which can still be a large number. IBR generally caps payments at 10% or 15% depending on when you first borrowed, making it a more manageable plan for most families. The one-ICR-payment rule is your ticket to the better plan.

A few things parents get wrong about consolidation:

Consolidation does not combine your loan with your child’s loans. It only applies to your Parent PLUS loans.

You do not lose your payment history toward forgiveness programs when you consolidate correctly.

The double consolidation loophole that some borrowers previously used to access IBR more quickly is no longer necessary. A single consolidation with one ICR payment now unlocks IBR directly under current rules.

Pro Tip: The consolidation process can take 30 to 90 days from application to disbursement. Submit your application well before any deadlines to avoid getting cut off from the IDR access you need.

Critical 2026 deadlines every parent must know

This is where urgency becomes real. The rules around repayment plans for Parent PLUS are changing in a significant way, and missing the upcoming deadlines has permanent consequences.

Your Direct Consolidation Loan must be disbursed by June 30, 2026 to preserve your eligibility for income-driven repayment plans. Loans disbursed after that date fall under the Tiered Standard Repayment Plan, which lasts 10 to 25 years depending on your balance, with no income adjustments and no forgiveness path.

Because processing can take up to 90 days, applications should be submitted by April 1, 2026 to give your servicer enough time to disburse before the cutoff. If you are still thinking about it, that window is very narrow.

Here is a comparison of what you can access before and after the deadline:

Repayment benefit | Before July 1, 2026 disbursement | After July 1, 2026 disbursement |

Income-driven repayment (ICR/IBR) | Available after consolidation | Not available |

PSLF eligibility | Available | Not available |

Forgiveness after 20 to 25 years | Available under IDR | Not available |

Tiered Standard Plan | Not applicable | Mandatory |

There is a second trap many parents do not see coming. Taking out any new Parent PLUS loan on or after July 1, 2026 will force all of your existing Parent PLUS loans into the Tiered Standard Plan. This means a single borrowing decision for a younger child could erase the IDR and forgiveness progress you have already built for an older child’s loans.

Pro Tip: If you have a younger child starting college after mid-2026, explore alternatives to Parent PLUS loans first, such as additional unsubsidized loans in the student’s name or private parent loans. Taking on new federal Parent PLUS debt after the deadline could cost you your forgiveness eligibility entirely.

Parent PLUS loan forgiveness: your realistic options

Parent PLUS loan forgiveness is real, but it requires you to complete the consolidation steps above first. Here is what is available once you are enrolled in an IDR plan:

Public Service Loan Forgiveness (PSLF): If you work full-time for a qualifying employer such as a government agency, nonprofit, or public school, you may qualify for forgiveness after 120 qualifying payments under an eligible IDR plan. That is 10 years of payments.

IDR forgiveness after 20 to 25 years: If you are not in public service, forgiveness is still possible after making 20 or 25 years of qualifying payments under IBR or ICR.

Employment requirements for PSLF: The forgiveness applies to the borrower, which is you as the parent. Your employer must be a qualifying organization, not your child’s.

A few pitfalls to avoid:

Do not assume PSLF applies automatically after consolidation. You must submit an employer certification form regularly and track your qualifying payments.

Standard 10-year repayment rarely qualifies for PSLF because the loan is paid off before 120 payments accumulate under an IDR plan. You need IDR enrollment.

Missing a recertification deadline for your income-driven plan can result in payments that no longer count toward forgiveness.

You can learn more about these forgiveness pathways for parents through Titanprep’s guides, which break down PSLF eligibility in plain language.

Refinancing and other strategies to manage payments

Private refinancing is one of the most frequently discussed Parent PLUS loan refinancing options, and it genuinely helps some borrowers. But it comes with trade-offs that are easy to overlook when an attractive interest rate is on the table.

Refinancing into a private loan can lower your rate and shorten your repayment term, which reduces the total interest you pay. Some lenders also allow you to refinance the debt into your child’s name, which shifts the legal responsibility for the loan. This can make sense if your child is financially stable and willing to take it on.

The downside is significant. Once you refinance into a private loan, you permanently lose access to:

Income-driven repayment plans (ICR and IBR)

Public Service Loan Forgiveness

Federal deferment and forbearance options

Any IDR forgiveness after 20 to 25 years

Refinancing makes the most sense if you have a strong income, no interest in forgiveness programs, and a clear plan to pay off the balance quickly. If you are counting on PSLF or IBR forgiveness, refinancing is almost certainly the wrong move.

One strategic option before the July 1, 2026 deadline: if you have not yet consolidated, you can maximize borrowing under the current rules and consolidate all existing Parent PLUS loans before the cutoff. After that point, explore budgeting strategies to keep your IDR payments manageable year over year.

My take on navigating these changes

I have watched many parents discover the consolidation deadline too late, often because their loan servicer never mentioned it proactively. That is not a minor oversight. Missing June 30, 2026 means permanently losing access to income-driven repayment and forgiveness options, sometimes on balances of $80,000 or more.

What concerns me most is what I call the new loan trap. A parent who consolidates correctly and builds two years of qualifying PSLF payments can undo all of that progress by taking out one additional Parent PLUS loan for a younger sibling after July 1, 2026. The rules are unforgiving on this point.

My recommendation is simple: act now, not later. Submit your consolidation application before April 2026. If you work in public service, start tracking your payments immediately. And if you are considering whether to borrow more for a second child, weigh that decision very carefully against what you stand to lose on the first child’s loan.

The good news is that you are not alone in this. Forgiveness and affordable repayment are genuinely available to Parent PLUS borrowers who move before the deadline. The path is clear. You just have to take it.

— Ellis

How Titanprep can help you stay on track

Keeping up with consolidation deadlines, IDR applications, and forgiveness certifications is a lot to manage on your own. Titanprep is a document preparation and support service that helps parents like you organize and submit the paperwork required for federal programs like IDR and PSLF. Titanprep is not affiliated with the U.S. Department of Education, but the service is built specifically to reduce the administrative burden that causes so many borrowers to miss critical deadlines.

You can learn exactly how the process works on the Titanprep How It Works page, or browse the latest policy changes that affect your loans through important student loan updates. If you are unsure where you stand, start there. Early action is the best action you can take right now.

FAQ

What are the repayment options for Parent PLUS loans?

Parent PLUS loans offer Standard, Graduated, and Extended repayment plans without consolidation. After consolidating into a Direct Consolidation Loan, you can also access Income-Contingent Repayment and Income-Based Repayment plans.

Can Parent PLUS loans be forgiven?

Yes. After consolidation and enrollment in an eligible income-driven plan, Parent PLUS borrowers can qualify for Public Service Loan Forgiveness after 120 qualifying payments, or IDR forgiveness after 20 to 25 years of payments.

What is the 2026 Parent PLUS consolidation deadline?

Your Direct Consolidation Loan must be disbursed by June 30, 2026, to preserve access to income-driven repayment plans. Because processing takes up to 90 days, most experts recommend submitting your application by April 1, 2026.

Does refinancing a Parent PLUS loan make sense?

Refinancing into a private loan can lower your interest rate but permanently removes access to federal income-driven repayment plans and forgiveness programs. It works best for borrowers who do not need federal protections and want to pay off debt quickly.

What happens if I take out a new Parent PLUS loan after July 1, 2026?

Any new Parent PLUS loan borrowed on or after July 1, 2026, will force all of your existing Parent PLUS loans into the Tiered Standard Repayment Plan, removing your IDR and Public Service Loan Forgiveness eligibility permanently.

Recommended

Comments