How to qualify for forgiveness: Your federal loan guide

- TitanPrep Official

- May 26

- 9 min read

Figuring out how to qualify for forgiveness on your federal student loans is harder than it should be. The rules are specific, the paperwork is easy to miss, and one wrong step can delay your forgiveness by months or longer. Many borrowers spend years making payments, only to discover they were on the wrong repayment plan or working for the wrong type of employer. This guide walks you through the forgiveness eligibility criteria for Public Service Loan Forgiveness (PSLF) and Income-Driven Repayment (IDR) forgiveness, step by step, so you know exactly what to do and when.

Table of Contents

Key Takeaways

Point | Details |

Direct loans only | Only federal Direct Loans or consolidated loans qualify for forgiveness programs like PSLF. |

Annual certification | Submit employment certification forms annually and when switching employers to maintain eligibility. |

Qualifying employers matter | You must work full-time for a qualifying government or nonprofit employer to count payments. |

Make 120 qualifying payments | Payments must be made on time, in full, under a qualifying IDR plan for PSLF eligibility. |

Forgiveness is not automatic | Active management including certification and recertification is necessary to successfully receive forgiveness. |

Understanding federal student loan forgiveness basics

Before you take any action, you need to know which loans and which situations actually qualify. This is where many borrowers go wrong.

The loan type matters more than most people realize. Only federal Direct Loans qualify for PSLF, and income-driven repayment plans are required. If you have Federal Family Education Loan (FFEL) Program loans or Perkins Loans, you are not automatically eligible. You would need to consolidate them into a Direct Consolidation Loan first, which has its own consequences we will cover shortly.

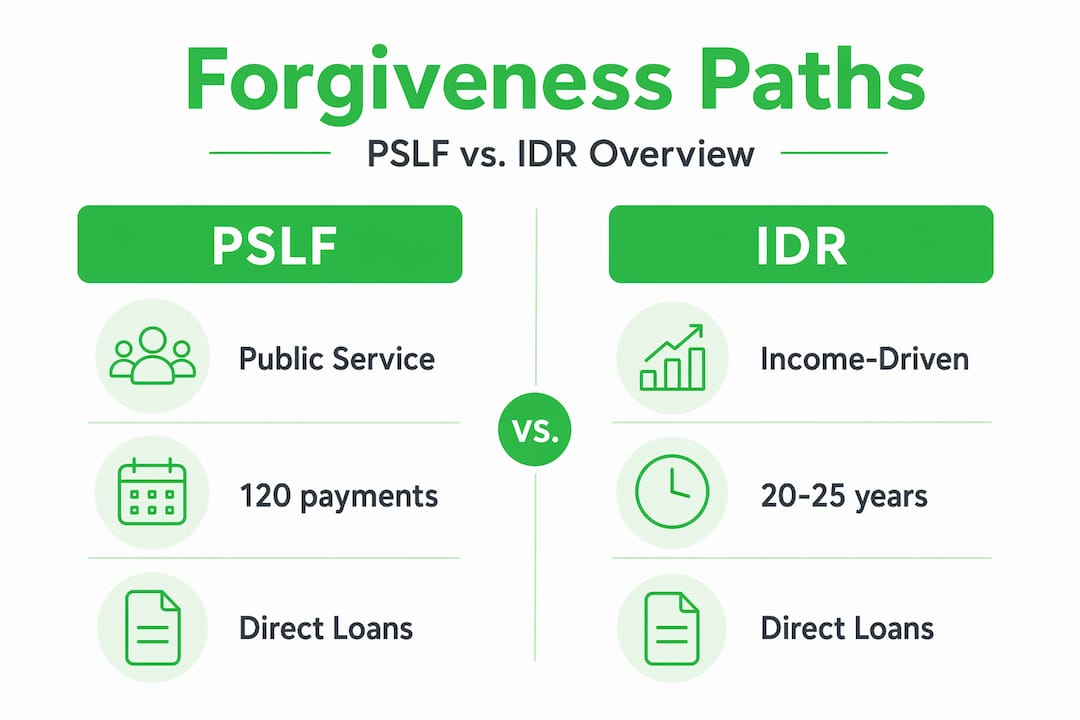

Here is a quick breakdown of the core forgiveness eligibility criteria for both major programs:

Requirement | PSLF | IDR forgiveness |

Loan type | Direct Loans only | Direct Loans only |

Repayment plan | IDR plan required | IDR plan required |

Payment count | 120 qualifying payments | 240 or 300 payments |

Employer type | Government or 501©(3) nonprofit | Any employer |

Employment status | Full-time required | No requirement |

Forgiveness timeline | After 10 years | After 20 or 25 years |

Who qualifies for forgiveness under PSLF specifically? You need to work full-time for a qualifying employer. That includes federal, state, local, or tribal government agencies and any 501©(3) nonprofit organization. Private companies, even those doing public good, generally do not count unless they hold the right tax-exempt status.

Key forgiveness program guidelines to keep in mind:

You must be enrolled in a qualifying student loan repayment plan, specifically an IDR plan

Payments must be on time, in the correct amount, and made while you are employed full-time

Income-driven repayment requires annual income recertification to maintain eligibility

Missing your annual recertification can cause your payment amount to spike and disqualify months from counting

Both programs require active management throughout the process, not just at the end

Pro Tip: If you are unsure whether your employer qualifies for PSLF, use the PSLF Help Tool on the Federal Student Aid website. It can verify employer eligibility before you commit years of payments to a path that may not pay off.

Getting this foundation right is critical. Reviewing federal student loan forgiveness guidance as policies update can also help you stay current with any changes that affect your eligibility.

Preparing to qualify: What you need and how to get ready

With a strong grasp of the qualifications, let’s explore the precise steps you need to take to prepare your application and documentation.

Preparation is the most underestimated phase of the forgiveness process. Most borrowers focus on making payments, but the groundwork you lay early determines whether those payments actually count.

Here is what you need to do before your payments even begin:

Confirm your loan type. Log into studentaid.gov and check whether your loans are Direct Loans. If they are not, you will need to consolidate before your payments can count toward forgiveness.

Consolidate if necessary, but carefully. Consolidation can make non-Direct loans eligible but resets your payment count and must be managed carefully. Every payment you made before consolidation no longer counts. This is a trade-off you need to understand fully before proceeding.

Select the right IDR plan. Your options include SAVE, PAYE, IBR, and ICR. Each has different eligibility rules and payment calculations. Your choice affects both your monthly payment amount and your forgiveness timeline.

Submit your first Employment Certification Form (ECF). Do not wait. Submit ECFs annually and whenever you change employers. Most borrowers mistakenly wait until they reach 120 payments, which can lead to major surprises if previous employers or payments are rejected.

Set up a tracking system. Keep records of every payment, every ECF submission, and every communication with your loan servicer. These records protect you if disputes arise.

What to gather when certifying your employment:

Your employer’s Employer Identification Number (EIN)

Proof of full-time employment status (30+ hours per week)

Your employer’s signature on the ECF

Documentation confirming your employer’s qualifying status

Pro Tip: Change jobs mid-year? Submit an ECF for your old employer before you leave, then submit another one for your new employer as soon as you start. Gaps in certification are one of the most common reasons payments get rejected.

When you are ready to apply for student loan forgiveness, having all of this documentation organized in advance makes the process significantly smoother. You should also review your options to lower your monthly payments if your current IDR plan is not the right fit.

Executing your forgiveness plan: Steps to qualify and apply

Now that you know how to prepare, let’s look at the exact steps to take to qualify and apply properly for forgiveness.

Execution is where discipline matters most. The forgiveness application process is not a single event. It is a multi-year commitment with specific rules that must be followed consistently.

Follow these steps to stay on track:

Enroll in a qualifying IDR plan before making your first payment.

Begin making on-time, full payments each month. Payments must be made after October 1, 2007 and while employed full-time by a qualifying employer. Partial payments and late payments do not count.

Submit your ECF every year, even if nothing has changed. Annual submission keeps your payment count verified and prevents retroactive rejections.

Recertify your income annually under your IDR plan. Missing this step can cause your payment to jump to a standard repayment amount, which may still count toward PSLF but could affect your budget significantly.

Reach 120 qualifying payments (for PSLF) or the required payment count for IDR forgiveness. For IDR, forgiveness requires 20 to 25 years of continuous payments, depending on your loan type and plan.

Submit your PSLF application once you hit 120 payments. This is a separate step from the ECF and must be completed to trigger forgiveness.

Here is a side-by-side look at the forgiveness timelines for IDR plans:

IDR plan | Forgiveness timeline | Best for |

SAVE | 20 years (undergrad) / 25 years (grad) | New borrowers with undergrad debt |

PAYE | 20 years | Borrowers with high debt-to-income ratio |

IBR (new borrowers) | 20 years | Borrowers who entered repayment after 2014 |

IBR (older borrowers) | 25 years | Borrowers who entered repayment before 2014 |

ICR | 25 years | Parent PLUS borrowers after consolidation |

“The forgiveness application process requires consistent action over many years. Understanding the requirements for forgiveness programs before you start protects every payment you make.”

Be aware of some critical pitfalls in this phase:

Making extra payments does not accelerate PSLF. You need 120 separate qualifying monthly payments, not a higher total dollar amount.

Refinancing federal loans into private loans immediately disqualifies you from all federal forgiveness programs.

Always verify that your servicer has recorded each payment correctly.

Understanding PSLF and teacher loan forgiveness details is also worth your time if you work in education, since teachers have access to additional programs. And stay cautious: knowing how to spot student loan forgiveness scams can protect you from losing money to bad actors.

Verifying your progress and avoiding common pitfalls

Having executed your application and payment strategy, next we explore how to verify your progress and troubleshoot common issues.

Verification is not optional. Forgiveness is not automatic. You need to actively confirm that your payments are counting and that your account is in good standing.

Here is what to monitor regularly:

Check your qualifying payment count through the PSLF Help Tool at least once per year

Review your loan servicer’s records for any discrepancies in payment amounts or dates

Confirm that each ECF has been processed and accepted, not just submitted

Watch for any changes to your IDR plan status, particularly after income recertification

“The most common mistake is assuming forgiveness is automatic without active account management including annual certification.”

One issue that catches many borrowers off guard: your income can work against you. If your income rises significantly, your IDR payment may eventually cover your full loan balance before the forgiveness timeline ends. In that case, forgiveness may not be guaranteed if your income increases significantly before the forgiveness timeline. Plan your career trajectory with this in mind, especially if you are pursuing IDR forgiveness over 20 or 25 years.

Pro Tip: If your servicer records a payment incorrectly, dispute it in writing immediately and keep a copy. Verbal corrections rarely hold up. Document everything.

Additional steps to protect your progress:

Save copies of every ECF and every loan servicer communication

Set calendar reminders for your annual income recertification deadline

Avoid forgiveness scams that promise fast-tracked results for a fee

Review whether you may qualify for DOE forgiveness programs based on your school or borrower circumstances

Why proactive management is the key to successful federal student loan forgiveness

Here is something most forgiveness articles will not tell you: the borrowers who fail to get forgiveness usually do not fail because they picked the wrong program. They fail because they were passive.

The federal forgiveness system was not designed to catch your mistakes. It does not send you a reminder when your income recertification is overdue. It does not flag a rejected ECF from three years ago. If you wait until you are close to the 10-year PSLF mark to sort out your records, you may discover that dozens of your payments did not count, and fixing that retroactively is a long, difficult process. Annual employment certification is recommended specifically to avoid complex audits at forgiveness time.

Consolidation is another area where passive borrowers get hurt. Consolidating when you do not need to resets your payment count. Not consolidating when you should means your loans stay ineligible. Neither outcome is good, and the system will not tell you which path is right for your situation.

Borrowers pursuing discharge options, like Total and Permanent Disability discharge, face a different kind of challenge. The documentation requirements are significant, and persistence matters. But this path remains a real and important option for borrowers who qualify. Understanding the full range of student loan discharge pathways puts you in a much stronger position regardless of your circumstances.

The bottom line is this: treat your forgiveness pursuit like a long-term project with real milestones. Review your account every year. Update your certifications on schedule. Keep records from day one. The borrowers who get forgiveness are almost always the ones who stayed engaged throughout the entire process, not just at the finish line.

How TitanPrep supports your journey to student loan forgiveness

Navigating forgiveness programs means managing years of paperwork, deadlines, and servicer communications. TitanPrep is a document preparation and support service built specifically for federal student loan borrowers who want to stay organized and avoid costly mistakes. We help you prepare and submit applications for IDR, PSLF, and eligible discharge programs, and we keep track of your documents and deadlines so nothing falls through the cracks. Stay current with important student loan updates, download a federal student loan forgiveness guide tailored to your situation, or walk through our student loan forgiveness application guide to understand exactly what comes next. TitanPrep does not guarantee outcomes, but we make sure you show up prepared.

Frequently asked questions

What types of federal loans qualify for Public Service Loan Forgiveness?

Only federal Direct Loans or Direct Consolidation Loans qualify for PSLF. FFEL and Perkins Loans must be consolidated into a Direct Consolidation Loan first before any payments can count.

How often do I need to certify my employment for PSLF?

You should submit the ECF annually and every time you change employers to keep your payment count accurate and avoid surprises when you apply for forgiveness.

Can I get student loan forgiveness if I have a disability?

Yes. Total and Permanent Disability discharge is available if you have a qualifying medical condition verified by the Social Security Administration, the Department of Veterans Affairs, or a licensed physician who meets specific criteria.

Does income affect eligibility for PSLF?

There is no income requirement for PSLF, but your income determines your monthly payment under an IDR plan, which in turn affects how much of your remaining balance gets forgiven after 120 payments.

What happens if I miss a payment or certification deadline?

Missing one PSLF requirement for any given month means that month does not count toward your 120 qualifying payments, effectively extending your forgiveness timeline by at least one month for each missed requirement.

Recommended

Comments