Temporary Expanded PSLF: Maximize your loan forgiveness

- TitanPrep Official

- May 11

- 9 min read

Getting denied for Public Service Loan Forgiveness (PSLF) can feel like the end of the road after years of public service and careful payments. But a PSLF denial is not always the final word. The Temporary Expanded PSLF program, commonly known as TEPSLF, exists specifically to give eligible borrowers a second chance at forgiveness when the only reason their PSLF application failed was the type of repayment plan they used. This article covers everything you need to know, from what TEPSLF is and whether you qualify, to exactly how to apply and what to watch out for along the way.

Table of Contents

Key Takeaways

Point | Details |

TEPSLF is a second chance | Borrowers denied PSLF due to repayment plan may still qualify for forgiveness via TEPSLF. |

Eligibility requires prior PSLF denial | You must have been denied PSLF for repayment plan reason and meet all other PSLF criteria. |

Apply digitally with employer signature | Use StudentAid.gov’s PSLF Help Tool for streamlined application and tracking. |

Funds are limited | TEPSLF operates on a capped budget, so acting quickly increases your chances. |

What is Temporary Expanded PSLF?

TEPSLF is a federal relief program created to fix a gap that caught thousands of borrowers off guard. Many public service workers made a decade’s worth of payments and worked faithfully at qualifying employers, only to discover that their repayment plan was not eligible for standard PSLF. That single administrative mismatch disqualified years of effort.

Congress responded by enacting TEPSLF in 2018. The program is a limited one-time program with up to $350 million set aside specifically to forgive loans for borrowers who would have qualified for PSLF in every other way. The funding is allocated on a first-come, first-served basis.

The core purpose of TEPSLF is narrow and intentional. It targets borrowers who made 120 payments while employed full-time at a qualifying public service employer, such as a government agency or a 501©(3) nonprofit, but were denied standard PSLF solely because their payments were made under a graduated or extended repayment plan rather than an income-driven repayment (IDR) plan.

Understanding this distinction is critical. TEPSLF is not a general do-over for any type of PSLF denial. It is specifically designed for one scenario: the right employer, the right number of payments, the wrong repayment plan. If your denial was caused by something else, such as loan type or employment classification, TEPSLF may not resolve your situation on its own.

“TEPSLF is not a fallback for every PSLF denial. It is a precise remedy for one specific mistake, and knowing that distinction can save you months of confusion and misapplied effort.”

Here is a quick comparison to help you see where TEPSLF fits among the broader student loan forgiveness programs available today:

Feature | PSLF | TEPSLF |

Repayment plan required | IDR plans only | Graduated or extended plans also count |

Funding | Unlimited (ongoing) | Capped at $350 million |

Application method | PSLF Help Tool | Same PSLF Help Tool, combined form |

Still available in 2026? | Yes | Yes |

Prior PSLF denial required | No | Yes |

Eligibility requirements for TEPSLF

Now that you understand what TEPSLF is, let’s see if you qualify. The eligibility requirements are more specific than PSLF, and getting each one right is essential before you invest time in the application process.

To qualify for TEPSLF, you must meet all of the following conditions:

You were previously denied for PSLF. TEPSLF is only available after a formal PSLF denial. If you have not yet applied for PSLF, you need to do that first.

Your denial was due to repayment plan type. The denial must have been because your payments were on a non-qualifying repayment plan, not for any other reason like loan type or employer eligibility.

You made 120 qualifying payments. These must have been made while working full-time at a qualifying employer, the same standard as PSLF.

Your recent payments meet IDR-level requirements. Even if your overall repayment history included graduated or extended plans, TEPSLF still requires that the payments in the 12 months before you applied were at least equal to what you would have paid under an IDR plan.

You were employed full-time during qualifying payments. Part-time employment does not count, even if you worked multiple jobs that together added up to full-time hours.

Several edge cases are worth knowing about. Deferment and forbearance periods generally do not count toward your 120 payments. There is one notable exception: COVID-19 forbearance may qualify depending on your circumstances. This distinction matters if you paused payments during 2020 or 2021 and are trying to calculate whether you have reached 120 payments.

Also important is the requirement to resolve any other PSLF denial reasons before TEPSLF can help you. For example, if your loans were in the wrong type of program, consolidating into a Direct Loan first may be a necessary step. Review your PSLF eligibility steps carefully before submitting anything under TEPSLF.

Teachers face a specific nuance. If you are both a teacher and a public service employee, you may qualify for more than one program. Understanding how TEPSLF interacts with teachers loan forgiveness can help you maximize what you receive without accidentally disqualifying yourself from either benefit.

Pro Tip: Pull your payment history from your loan servicer before you apply. Count each qualifying payment against the 120 required and confirm that your last 12 months of payments meet the IDR-equivalent amount. This preparation alone can prevent unnecessary delays.

Comparing TEPSLF vs. PSLF and limited waivers

If you’re confused by different forgiveness programs, here’s how TEPSLF stacks up against the others you may have heard about.

The most important thing to understand is the difference between TEPSLF and the limited PSLF waiver. The limited PSLF waiver was a temporary policy introduced in October 2021 and extended through October 2022. It was significantly more flexible than either standard PSLF or TEPSLF, allowing a wider range of loan types and repayment plans to count toward forgiveness. That waiver has now expired. If you did not apply before its deadline, you cannot access those benefits retroactively. You can learn more about the original DOE waiver announcement to understand what was covered and how it differed.

TEPSLF, by contrast, is still active. While TEPSLF is temporary with capped funding, there are currently no reports that its $350 million has been fully exhausted, which means eligible borrowers who act now may still be able to access it.

Here is a structured comparison of the three programs:

Program | Still available? | Repayment flexibility | Requires prior denial? |

PSLF | Yes | IDR plans only | No |

TEPSLF | Yes | Graduated and extended | Yes |

Limited PSLF waiver | No (expired) | Very flexible | No |

One more factor to consider involves recent 2025 to 2026 PSLF changes. The Department of Education narrowed the scope of qualifying employers by excluding those with a “substantial illegal purpose” effective July 2026. This change primarily affects employer eligibility going forward and does not directly alter how TEPSLF works. Importantly, any payment credits you have already earned under PSLF or TEPSLF remain protected under current guidance.

Here is a clear summary of key differences you should know:

PSLF is an ongoing program with no funding cap and accepts new applicants continuously.

TEPSLF has a fixed funding pool and is processed on a first-come, first-served basis.

The limited PSLF waiver is expired and no longer accepts applications.

Employer eligibility rule changes in 2026 affect PSLF going forward but do not erase existing qualifying payment counts.

TEPSLF requires that you have already been denied PSLF, making it a sequential process, not a parallel one.

Understanding these differences helps you avoid applying to the wrong program, which can cost you months of processing time.

How to apply for TEPSLF: Step-by-step guide

Once you know you’re eligible, here’s how to start your TEPSLF application. The good news is that TEPSLF does not require a completely separate application from PSLF. The same tool and the same form are used for both.

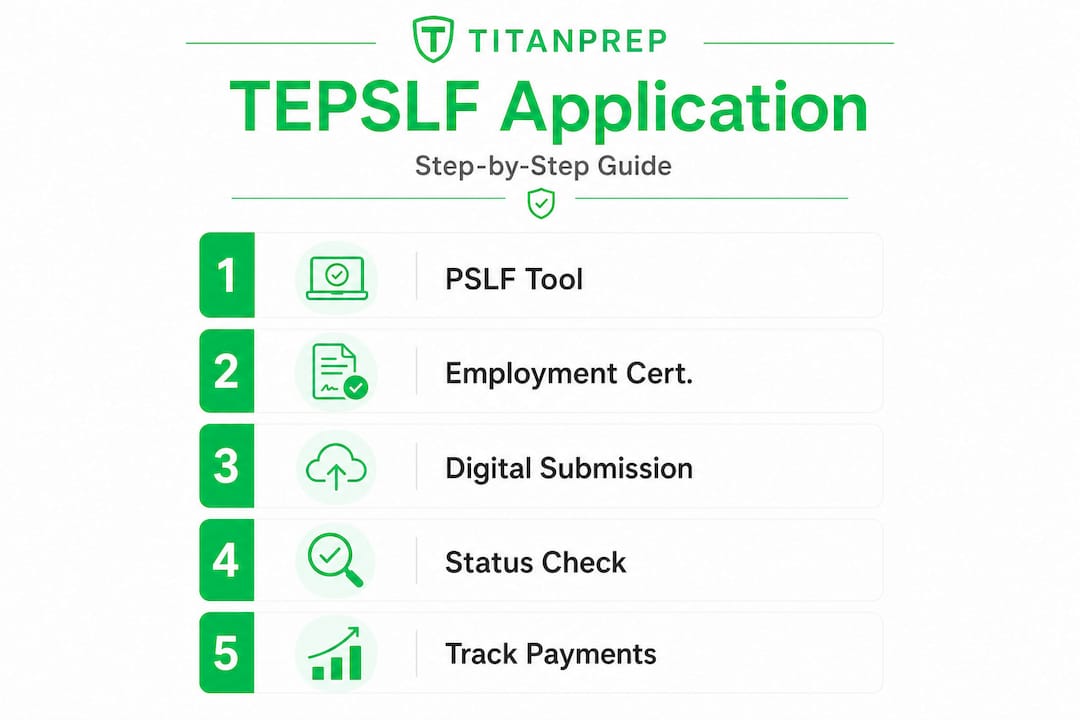

Step 1: Use the PSLF Help Tool on StudentAid.gov

The PSLF Help Tool generates a combined PSLF and TEPSLF form. When you go through the tool, it will assess your situation and automatically include TEPSLF consideration if you qualify. This makes the process simpler than many borrowers expect.

Step 2: Complete employment certification

Your employer must sign the combined form. This certifies that you were employed full-time at a qualifying public service organization during the periods you are claiming. Getting employer signatures can take time, especially at large government agencies or hospitals, so start this process early.

Step 3: Submit the form digitally

Once signed, submit your completed form through StudentAid.gov. Digital submission is preferred and faster than mail. Keep a copy for your records and note the date and confirmation number from your submission.

Step 4: Monitor your application status

After submission, log back into the PSLF Help Tool periodically to check your status. Your loan servicer may also send follow-up requests for additional documentation. Respond promptly to avoid delays.

Step 5: Track your payment count

Over 1 million borrowers have now received PSLF approval through 2024 and 2025. Keeping your own count and confirming each qualifying payment against your records puts you in the best position to catch errors before they become problems. Review the latest ED guidance on PSLF to stay current on any policy updates that could affect your file.

Pro Tip: Submit an Employment Certification Form every year rather than waiting until you have made all 120 payments. Annual submission means errors are caught early, your employer history is verified while the details are fresh, and your payment count is confirmed on a regular basis.

Our perspective: Second chances and speed matter with TEPSLF

With the technical steps behind us, here’s the bigger lesson borrowers need to hear.

Most conversations about TEPSLF focus on eligibility checklists. That is important. But what often gets overlooked is the psychology of waiting. Many borrowers who were denied PSLF feel frustrated and discouraged, and they put off exploring TEPSLF because they assume the answer will be the same. That delay is a real risk.

Here is what we know from working with borrowers in this situation: the paperwork is manageable, but the hesitation is what costs people. TEPSLF funds are first-come, first-served. As of 2026, no reports indicate that the program’s funding has been depleted, but that does not mean it will stay that way indefinitely. Eligible borrowers who act now have a real opportunity. Borrowers who wait may not.

There is also a practical issue with timing that many people miss. The requirement that your most recent 12 months of payments meet an IDR-equivalent amount means that if you have stopped making payments or switched to a plan that does not meet that threshold, your TEPSLF eligibility could be affected. The clock does not simply stop while you wait to apply.

Our view is that TEPSLF deserves more urgency than it typically gets. It is easy to treat it as a “maybe later” option, but for borrowers who spent years in public service and made every payment in good faith, this program can mean tens of thousands of dollars in loan forgiveness. That outcome is worth acting on quickly.

If you have already earned PSLF credit or are working toward it, staying aware of your options around automatic PSLF forgiveness and TEPSLF together puts you in the strongest position possible. The programs are complementary, not competing, and understanding both gives you more control over your path forward.

Ready to maximize your forgiveness? Let TitanPrep help

If this guide clarified your TEPSLF path, here’s how TitanPrep can support your next move. Navigating the paperwork and deadlines for TEPSLF is manageable with the right support system. TitanPrep helps borrowers stay organized through every stage of the process, from preparing your PSLF and TEPSLF forms to tracking submissions and monitoring deadlines through our secure client portal. Learn how our process works and see how we can help you avoid the costly errors that often slow TEPSLF applications down. Access our loan forgiveness guide for deeper resources, and stay current with the latest student loan updates that could affect your eligibility. TitanPrep is not affiliated with the Department of Education, and we do not guarantee outcomes, but we are committed to helping you stay on track and submit with confidence.

Frequently asked questions

Is TEPSLF still available in 2026?

Yes, TEPSLF remains available in 2026 and there are currently no reports that its funding has been exhausted, though it remains first-come, first-served.

Who is eligible for TEPSLF?

Borrowers who made 120 payments while working full-time at a qualifying public service employer, were denied PSLF only because of their repayment plan type, and otherwise meet all PSLF requirements may be eligible.

Does a period of deferment or forbearance count toward TEPSLF?

Generally, deferment or forbearance periods do not count toward the required 120 payments, though COVID-19 forbearance may be an exception depending on your circumstances.

How do I apply for TEPSLF?

Use the PSLF Help Tool on StudentAid.gov, which generates a combined PSLF and TEPSLF form, then submit it digitally with your employer’s signature to begin the review process.

Recommended

Comments