How to change your federal student loan repayment plan

- TitanPrep Official

- May 15

- 9 min read

Changing your federal student loan repayment plan is not as complicated or costly as many borrowers assume. A lot of people believe the process is reserved for those in financial crisis, or that it involves fees similar to refinancing. In reality, for federal loans, switching plans is typically free, flexible, and can be initiated at almost any time. Whether your income has changed, you’re aiming for loan forgiveness, or you simply want a lower monthly payment, understanding how repayment plan changes work can open the door to real financial relief.

Table of Contents

Key Takeaways

Point | Details |

Not all plans are equal | Eligibility and outcomes vary by plan, so compare carefully before submitting a change. |

Plan changes are free | Most federal borrowers can change repayment plans at no cost by working with their loan servicer. |

Process takes time | It can take several weeks for a change to take effect, and payments may stay the same during processing. |

Plan impacts vary | Switching plans can affect monthly payments, total interest, and forgiveness eligibility. |

Review plans yearly | Regularly checking your options helps you get the best fit as your life and rules change. |

What is a repayment plan change?

A repayment plan change means officially requesting to move from one federal student loan repayment option to another. That’s it. You’re not taking out a new loan, you’re not refinancing, and you’re not starting over. You’re simply telling your loan servicer that you want a different payment structure.

For federal student loans, a “repayment plan change” means submitting a request to move from one repayment plan to another, such as switching from a Standard plan to an Income-Driven Repayment (IDR) plan. Borrowers do this for many reasons:

Financial hardship: Your income dropped, and you need a lower monthly payment.

Career change: You started a public service job and want to pursue Public Service Loan Forgiveness (PSLF).

Income increase: You want to pay loans off faster and move to a plan with higher payments.

Loan forgiveness strategy: You want to qualify for forgiveness after 20 or 25 years under an IDR plan.

The main categories of federal repayment plans include:

Standard Repayment: Fixed payments over 10 years.

Graduated Repayment: Payments start low and increase every two years.

Extended Repayment: Stretches payments over up to 25 years.

IDR Plans: Payments are based on your income and family size, with forgiveness after a set number of years.

Switching repayment plans is not the same as refinancing. Refinancing means taking out a new private loan to replace your federal loans, which can cause you to lose federal protections and forgiveness options. A plan change keeps your loans federal and intact.

If you’re still researching your options, start by comparing income-driven plans to see which one might suit your current situation. Different IDR plans have different formulas for calculating your payment, and some have stricter eligibility rules than others.

Eligibility and requirements for changing your plan

Now that you know what a repayment plan change is, you need to understand who qualifies and what factors shape your options. Not every borrower can switch into every plan, and knowing your eligibility upfront saves time and frustration.

Your repayment plan eligibility depends primarily on your loan type. Here’s a general breakdown:

Direct Loans are eligible for all federal repayment plans, including all IDR options.

Federal Family Education Loans (FFEL) may qualify for some plans but not all. Consolidating into a Direct Loan may open up more options.

Perkins Loans are generally not eligible for IDR plans without consolidation.

Parent PLUS Loans have limited IDR eligibility. They can only access the Income-Contingent Repayment (ICR) plan, and only after consolidation.

Beyond loan type, some plans have additional requirements:

Income documentation: Most IDR plans require proof of income, such as a recent tax return or pay stubs.

Family size certification: You’ll need to report your household size, which affects your payment calculation.

Loan status: Your loans generally must be in good standing or in an eligible repayment status.

Specific form submission: For IDR plans, you’ll submit an IDR Request form, which can be done online through Federal Student Aid or mailed to your servicer.

The process of changing plans through your servicer is plan-specific and paperwork-dependent. Edge cases matter here. You may not be able to switch into every plan you want because eligibility depends on factors like loan type and borrower status. Always verify eligibility before submitting any paperwork.

Pro Tip: Before submitting a plan change request, log into your Federal Student Aid account at studentaid.gov and review your loan types. This single step can prevent you from applying for a plan you’re not eligible for, which delays the process and adds unnecessary stress.

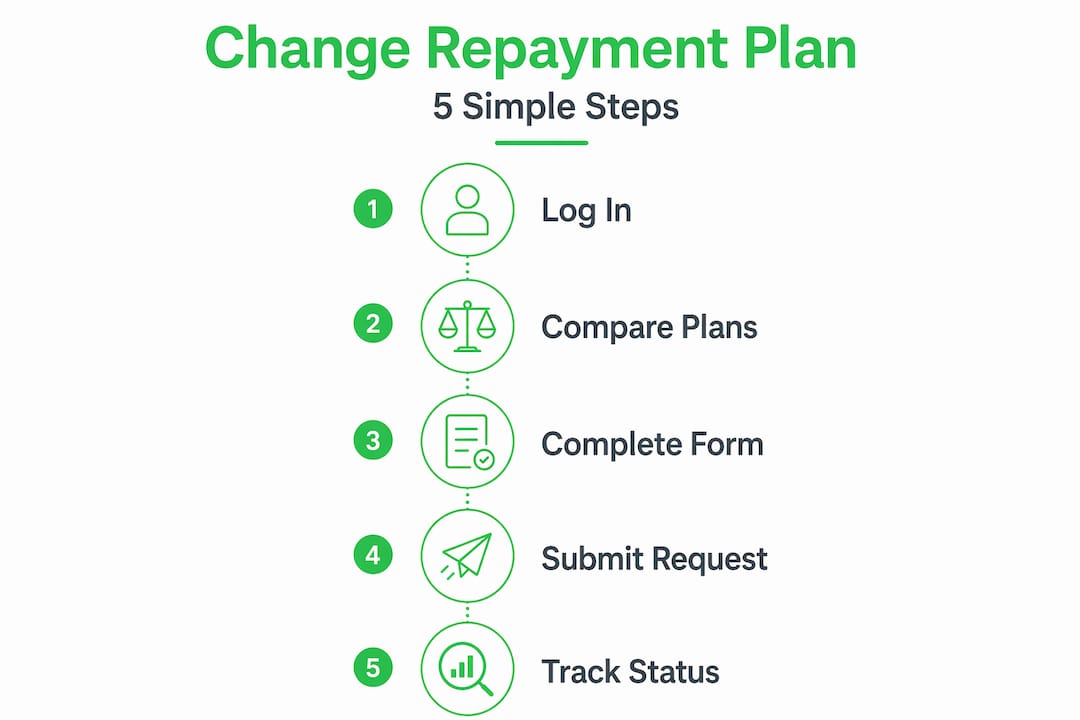

How does the process work?

Once you know you’re eligible, it’s time to walk through how the process actually works step by step. The good news is that for most borrowers, this is a manageable process that you can complete online in under an hour.

Borrowers generally can change federal student loan repayment plans through their loan servicer or loan holder rather than by refinancing. Here’s how to do it:

Log into your servicer’s website or contact them by phone. Common servicers include MOHELA, Aidvantage, and Nelnet.

Select your new plan. For IDR plans, you’ll complete the IDR Request form. For non-IDR plans like Graduated or Extended, your servicer may process the change with a simpler request.

Submit supporting documents. Income documentation is required for IDR plans. Upload tax returns, pay stubs, or use the IRS Data Retrieval Tool if available.

Wait for confirmation. Processing times vary, but most changes are completed within a few weeks.

Check your account to confirm the update has taken effect. Look for a new payment amount and updated repayment terms.

The account may remain on the previous payment amount and plan while the request is processed, so borrowers should plan for potential timing delays and verify the update with their servicer.

This timing gap matters. If your billing date falls before your new plan is processed, you might owe the old payment amount. Budget for this possibility. Also, some IDR switches result in a short-term forbearance during the transition phase, which temporarily pauses your payments while the plan is finalized.

Pro Tip: After submitting your request, keep a record of everything. Screenshot your submission confirmation, note the date you submitted, and save any email correspondence with your servicer. If there’s a dispute later, this documentation is invaluable.

Comparing repayment plans: Finding your best fit

Now that you know the process, the next step is choosing wisely. More than one repayment plan may be available for federal borrowers, and making an informed choice often involves using Federal Student Aid tools to compare outcomes.

Use the federal loan calculator on studentaid.gov to model what your payments would look like under each plan. This tool lets you plug in your income, family size, and loan balance to see projected monthly payments and total repayment costs side by side.

Here’s a simplified comparison to help you evaluate your options:

Plan | Payment basis | Loan term | Forgiveness available? | Best for |

Standard | Fixed amount | 10 years | No | Paying off quickly |

Graduated | Starts low, rises | 10 years | No | Early career borrowers |

Extended | Fixed or graduated | Up to 25 years | No | Large balances |

IDR (SAVE, PAYE, IBR, ICR) | % of discretionary income | 20 to 25 years | Yes | Lower incomes or forgiveness goals |

Key questions to ask yourself when comparing plans:

What can I afford monthly right now? A lower payment helps cash flow today but may cost more over time.

How long do I want to be in repayment? Shorter terms mean higher payments but less interest paid overall.

Am I pursuing forgiveness? If so, IDR plans are typically required for income-driven forgiveness, and PSLF requires an IDR-qualifying plan.

How stable is my income? If your income fluctuates, an IDR plan adjusts each year based on your latest information.

Also consider how budgeting for student loans fits into your broader financial picture. Your repayment plan should work alongside your other financial obligations, not against them.

Potential impacts of switching your repayment plan

Comparison is one thing. Understanding real-world impacts is the final step before making a change. Switching plans affects more than just your monthly bill.

When switching income-driven plans, borrowers may experience a transition period that can include forbearance depending on the direction of the switch. That short pause can feel like a relief, but it also means no payments are counting toward forgiveness during that time.

Here’s a summary of key impacts to keep in mind:

Impact area | Potential effect | What to watch for |

Monthly payment | May decrease or increase | Budget for the new amount before it kicks in |

Total interest paid | Lower payments often mean more interest over time | Use the loan simulator to compare totals |

Forgiveness progress | May or may not carry over | Confirm with your servicer before switching |

Processing delays | Possible billing gap | Keep making payments until change is confirmed |

Forbearance | Short-term pause possible during IDR switches | Forbearance months may not count toward forgiveness |

Additional things to keep in mind:

Switching from IDR to Standard will likely increase your payment and reduce your term, which saves on total interest but requires a bigger monthly commitment.

Switching from Standard to IDR can significantly lower your payment amount but may extend your repayment period and increase what you pay overall.

Switching between IDR plans can affect your qualifying payment count toward forgiveness. For example, moving between plans mid-repayment may or may not preserve your existing progress depending on program rules.

If you’re thinking about preparing for payment changes, now is the right time to review your full situation before committing to a new plan. Going in informed protects you from unpleasant surprises.

A smarter approach to repayment plan changes

You’ve seen the technical details. Here’s something most articles skip over.

Most borrowers ask one question when evaluating repayment plans: “What’s the lowest monthly payment I can get?” That focus is understandable. When money is tight, you want relief now. But minimizing your monthly payment without considering total repayment cost is one of the most common and costly mistakes borrowers make.

Here’s the reality. A lower monthly payment stretched over 25 years can mean you pay tens of thousands of dollars more in interest than you would on a 10-year plan. That’s not a scare tactic. That’s math. Before you optimize for monthly cash flow, run the numbers on total cost. You may find that a modest increase in monthly payments now leads to a dramatically lower lifetime cost.

The other mistake we see repeatedly is what we call “set it and forget it” repayment. A borrower switches to an IDR plan when their income is low, gets relief, and then never revisits the plan when circumstances change. Income rises. Family size shrinks. A better plan becomes available. But nothing gets updated because the borrower assumed it would handle itself.

Federal repayment programs reward active management. Recertifying your income annually, checking for new plan options each year, and using smarter budgeting strategies can make a real difference in how quickly you pay off your loans and how much you ultimately owe. Think of your repayment plan like a subscription you review once a year to make sure it still fits your needs.

The borrowers who come out ahead are the ones who stay engaged with their loans, not the ones who find the easiest option and walk away.

Need guidance on your repayment plan change?

Navigating repayment options is manageable with the right support, and you don’t have to figure it out alone. TitanPrep is a document preparation and support service that helps borrowers organize, prepare, and submit paperwork for federal student loan programs, including IDR applications and related requests. If you’re not sure which plan fits your situation or want help making sure your paperwork is complete and submitted correctly, we’re here to help. Learn how TitanPrep works and explore our student loan FAQs to find clear answers to common questions. Every borrower’s path is different, and having organized, accurate documentation is one of the most practical steps you can take toward staying on track.

Frequently asked questions

Can I change my federal student loan repayment plan at any time?

Yes, most federal loan borrowers can change plans anytime through their loan servicer at no cost, though processing times can vary.

Does changing my repayment plan affect my loan forgiveness?

Switching plans may reset progress toward certain forgiveness programs, so always confirm your plan’s rules with your servicer before making a change. Eligibility for forgiveness also depends on loan type and borrower status.

What documents do I need to change my repayment plan?

You typically need to complete a formal request form and may need to provide income documentation. The IDR request process is plan-specific, so check your new plan’s requirements before submitting.

How long does it take for a repayment plan change to go into effect?

Most changes process within a few weeks, but your account may remain on the previous payment amount until the update is fully applied, so verify the change with your servicer.

Is changing my repayment plan the same as refinancing?

No. Changing plans keeps your loans federal and is handled through your existing loan servicer, while refinancing creates a new private loan and eliminates federal protections.

Recommended

Comments