Budget Your Way to Student Loan Repayment Success

- TitanPrep Official

- Apr 29

- 10 min read

You just landed your first real job. The excitement fades fast when you realize that a significant portion of your paycheck is already spoken for before you buy groceries or pay rent. For most recent graduates, average balances reach $33,566 for borrowers aged 25 to 34, with monthly payments ranging from $200 to $393 depending on your plan. That is not a small number. The good news is that with a clear budget and a smart repayment strategy, you can stay on top of your loans, cover your essentials, and still build toward real financial stability.

Table of Contents

Key Takeaways

Point | Details |

Know your obligations | Understanding what you owe and your minimum payment is the first step to budgeting for student loan repayment. |

Build a realistic budget | Set up a budget with actual loan payments and essential living expenses so nothing catches you off guard. |

Match the right plan | Choose a repayment plan that fits your income and goals to avoid unnecessary stress and interest. |

Track and adjust | Regularly monitor your spending and debt progress to spot issues and adapt quickly. |

Balance payoff and life | Make steady progress on loans while also maintaining financial flexibility and enjoying new experiences as a graduate. |

Understanding your student loan obligations

Before you can build a budget that works, you need to know exactly what you owe and when you owe it. Many new grads skip this step and end up surprised by their first bill.

The average loan balance for bachelor’s degree graduates sits between $32,000 and $35,000. Your minimum monthly payment depends on which repayment plan you are enrolled in. If you do nothing after graduation, the federal government places you on the Standard Repayment Plan by default, which spreads payments over 10 years.

Here is a quick look at how common plans compare:

Repayment plan | Typical monthly payment | Loan term | Best for |

Standard (10-year) | $300 to $393 | 10 years | Stable income, want to pay off fast |

Extended | $150 to $250 | 25 years | Lower monthly cost, more interest overall |

Income-Driven (IDR) | $0 to $200 | 20 to 25 years | Low or variable income |

Graduated | $150 rising to $400+ | 10 years | Expects income growth |

Knowing your minimum payment is the foundation of your budget. It is a fixed obligation, much like rent. If you miss it, your credit score takes a hit and penalties add up fast. Be sure to stay current on loan payment changes in 2025 and the latest student loan updates, because federal policies shift and your payment amount may change.

Key facts to know about your loans:

Grace period: Most federal loans give you a 6-month grace period after graduation before payments begin.

Loan servicer: Your servicer is the company that collects your payments. Know who they are and how to contact them.

Interest rate: Federal undergraduate loans typically carry rates between 5% and 7%, depending on the year you borrowed.

Capitalized interest: If you defer payments, unpaid interest gets added to your principal balance, making the total you owe grow.

Understanding these basics puts you in control rather than reacting to surprises.

Preparing your budget: Tools, essentials, and real numbers

Once you know your minimum monthly loan obligation, it is time to build or adapt your budget so these payments fit in without crowding out everything else.

Research from the Federal Reserve found that payment resumption cut spending by roughly $12.20 per week for every $10,000 in student debt. That is real money out of your weekly spending. If you carry $35,000 in debt, you could see your discretionary spending drop by more than $42 per week. Planning for this impact is not optional. It is essential.

Step-by-step budget setup:

Calculate your net income. Start with your take-home pay after taxes and any employer deductions. This is your actual working number.

List fixed expenses first. Rent or mortgage, utilities, car payment, insurance, and your minimum student loan payment go here.

Estimate variable expenses. Groceries, gas, dining out, subscriptions, and personal care items are variable. Track these for one month to get accurate numbers.

Assign a savings target. Even $50 to $100 per month toward an emergency fund matters. Build this in from the start.

Calculate what is left. Whatever remains after fixed expenses, variable costs, and savings is your discretionary budget.

Here is a sample monthly budget for a graduate earning $3,500 net per month with a $393 loan payment:

Category | Monthly amount |

Rent | $1,100 |

Student loan payment | $393 |

Groceries | $300 |

Transportation | $200 |

Utilities and phone | $150 |

Emergency savings | $100 |

Personal care and subscriptions | $100 |

Discretionary spending | $157 |

Total | $2,500 |

Notice that $1,000 is still unaccounted for in this example. That gap is your opportunity to pay extra on loans, build savings faster, or handle irregular expenses like car repairs or medical bills. Check out budgeting resources for students for additional templates and tools.

Pro Tip: Use a free budgeting app like Mint or YNAB (You Need A Budget) to connect your bank accounts and automatically categorize spending. Seeing your numbers in real time makes it much easier to catch overspending before it becomes a problem.

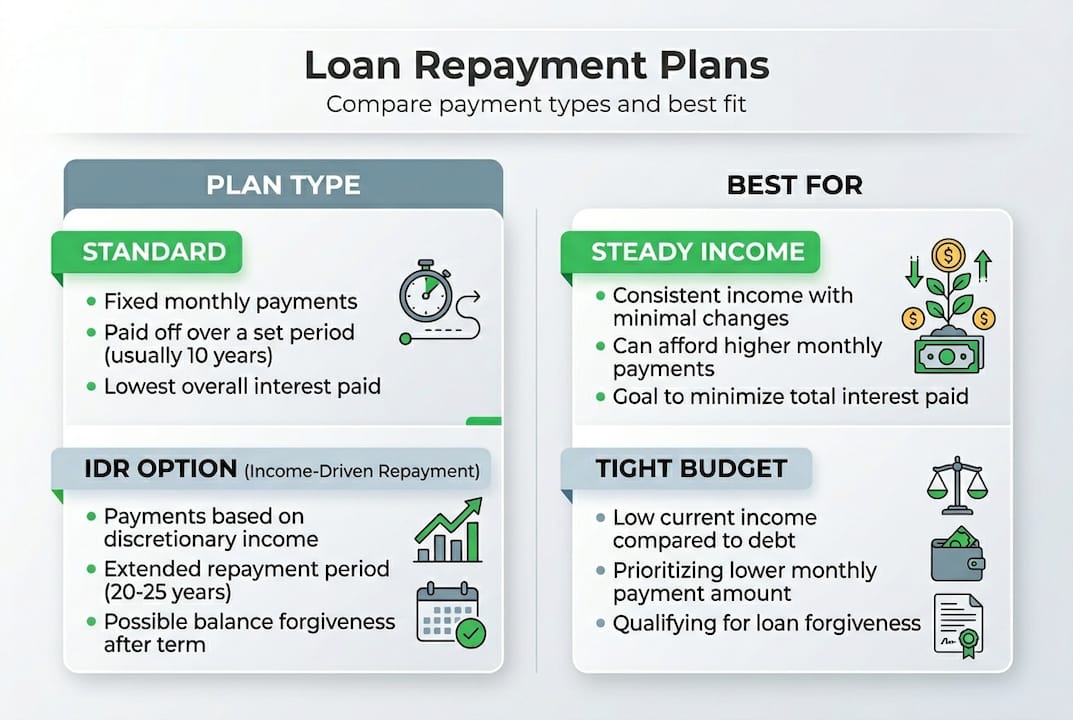

Choosing the right repayment plan for your situation

With your budget framework in place, you now need to pick a payment plan that matches your financial reality and long-term goals.

The two main categories are the Standard Repayment Plan and Income-Driven Repayment (IDR) plans. IDR plans calculate your payment as a percentage of your discretionary income, which means payments can be as low as $0 to $20 per month early in your career. According to repayment strategy research, IDR offers real advantages including credit protection and potential loan forgiveness after 20 to 25 years of qualifying payments.

However, IDR also has real drawbacks:

Higher total interest. Lower payments mean more time for interest to accumulate, so you often pay more over the life of the loan.

Negative amortization. If your payment does not cover monthly interest, your balance can actually grow even while you make payments.

Annual recertification. You must update your income and family size every year to stay enrolled. Missing this deadline can spike your payment.

Taxable forgiveness. Any forgiven balance after 20 to 25 years may be treated as taxable income after 2025, which could create a large tax bill.

Here is a direct comparison to help you decide:

Factor | Standard plan | IDR plan |

Monthly payment | Higher ($300 to $393) | Lower ($0 to $200) |

Total interest paid | Lower | Higher |

Loan term | 10 years | 20 to 25 years |

Forgiveness option | No | Yes |

Cash flow impact | Tighter | More flexible |

Annual recertification | No | Yes |

If your income is steady and covers your expenses comfortably, the Standard Plan saves you the most money over time. If your income is low or unpredictable, IDR gives you breathing room without risking default. You can also explore student loan forgiveness options if you work in public service or a qualifying nonprofit, which opens the door to Public Service Loan Forgiveness (PSLF) after 10 years of qualifying payments.

For personalized guidance on which plan fits your situation, consider reaching out for student loan repayment help. Policy changes happen frequently, so staying current on updates on loan forgiveness is also worth your time.

Pro Tip: You can switch repayment plans at any time for free. If your income drops or you face a financial hardship, contact your servicer and request a plan change rather than skipping payments.

Executing your repayment strategy: Monthly moves and cash flow fixes

After selecting your repayment plan, it is time to put your strategy into action and make monthly routines stick.

Consistency is what separates people who pay off loans on schedule from those who fall behind. Here is a practical monthly action plan:

Automate your payment. Set up autopay through your loan servicer. Most federal servicers offer a 0.25% interest rate reduction just for enrolling. That small discount adds up over 10 years.

Track your due dates. Add your payment due date to your phone calendar with a reminder three days before. This gives you time to transfer funds if needed.

Review your budget weekly. A five-minute check every Sunday to review spending keeps you aware of where your money is going.

Find one expense to cut each month. Canceling one unused subscription or cooking at home one extra night per week can free up $30 to $50 for extra loan payments.

Apply windfalls strategically. Tax refunds, work bonuses, or birthday money can go directly toward your loan principal. Even one extra payment per year shortens your payoff timeline noticeably.

Research on balancing aggressive payoff vs. liquidity shows that a hybrid approach works best for most borrowers. Pay the IDR minimum when cash is tight, and make extra principal payments when you have more room. This protects your cash flow while still reducing your balance over time.

“The goal is not to pay off your loans as fast as humanly possible. The goal is to build a financial life that is sustainable and growing, with loans as one manageable piece of it.”

Avoid these common budgeting mistakes that trip up new graduates:

Forgetting to budget for irregular expenses like car registration, dental visits, or holiday gifts

Treating credit cards as extra income rather than a short-term tool paid in full each month

Skipping your emergency fund because you want to pay more on loans

Learn more about common student loan mistakes so you can avoid the pitfalls that set many grads back by months or even years.

Measuring progress and troubleshooting setbacks

With routines established, monitoring your progress keeps you motivated and ready to respond if things get off track.

Tracking your debt payoff is about more than just watching the balance go down. It is about recognizing milestones that confirm your plan is working.

Key milestones to watch for:

Principal reduction. Your loan balance should decrease each month once you are past the interest. If it is not going down, you may be experiencing negative amortization.

Emergency fund growth. Aim for three to six months of expenses in a savings account. This cushion protects your loan payments during unexpected hardships.

Credit score improvement. On-time payments are the single biggest factor in your credit score. Consistent payments should lift your score over time.

Debt-to-income ratio drop. As your income grows and your balance falls, this ratio improves, which opens doors to better financial products like mortgages or car loans.

The Federal Reserve data confirms that student debt affects spending significantly, with roughly 17% of U.S. adults carrying student loans and the average borrower managing 2.2 types of debt simultaneously. You are not alone in juggling multiple financial obligations.

If you miss a payment, act quickly. Contact your servicer within the first 30 days. Loans become delinquent after one missed payment but do not go into default until 270 days of non-payment for federal loans. Options like forbearance or deferment can pause payments temporarily without damaging your credit. Stay informed about student loan payment trends so you know what changes may be coming.

Life changes fast in your twenties. A new job, a move to a different city, or a change in living situation all affect your budget. Revisit and revise your budget any time your income or expenses shift by more than $200 per month.

What most guides miss: The real-life balancing act in early repayment

Most articles about student loan repayment give you the same advice: pay as much as possible, cut every expense, and get out of debt fast. That advice is not wrong, but it is incomplete.

Hyper-aggressive repayment works on paper. In real life, it often leads to burnout, resentment, and eventually abandoning the plan entirely. If you cut every enjoyable expense from your life for five years, you are not just paying off loans. You are also delaying the experiences and connections that make your twenties meaningful.

The smarter approach is sustainable balance. That means setting a repayment pace that is ambitious but livable. It means budgeting for a concert ticket or a weekend trip without guilt, because those experiences are part of a healthy financial life, not the enemy of it.

We have seen borrowers who put every spare dollar toward loans for two years, only to hit a wall and start missing payments out of exhaustion. We have also seen borrowers on IDR plans who make minimum payments, live their lives, and still reach forgiveness or payoff on schedule. The difference is not the dollar amount. It is the consistency.

The hybrid approach, paying IDR minimums and adding extra payments when your budget allows, is often the most realistic and effective strategy for early-career borrowers. It keeps your credit clean, your cash flow healthy, and your motivation intact. Avoiding early budget burnout is just as important as avoiding missed payments.

Your financial health includes your mental health. A budget that leaves no room for enjoyment is a budget that will not last.

Take the next step: Expert student loan help and resources

Navigating repayment plans, forgiveness programs, and budget adjustments on your own can feel overwhelming. You do not have to figure it all out alone.

TitanPrep is a third-party service built specifically to help borrowers like you stay on track, avoid costly mistakes, and understand your options clearly. Whether you need help choosing a repayment plan or want to know if you qualify for forgiveness, we have resources ready for you. Start with our free federal loan forgiveness guide to understand what programs may apply to your situation. When you are ready for personalized support, get student loan help from our team and take the guesswork out of your repayment journey.

Frequently asked questions

What percentage of my income should go toward student loan payments?

Aim to keep debt payments under 10 to 15% of your take-home pay if possible, adjusting for essential expenses and financial goals. If your loans push you above that threshold, an income-driven repayment plan can help bring payments into a manageable range.

How can I cover other expenses if most of my budget goes to student loans?

Consider income-driven repayment to lower your monthly payment, then rework your budget to prioritize essentials while exploring additional income sources or spending cuts. Even small adjustments to discretionary spending can free up meaningful room in your monthly budget.

What if I miss a student loan payment while following my budget?

Contact your servicer immediately and review options such as forbearance, deferment, or switching to a lower-payment plan to avoid credit damage. Acting within the first 30 days gives you the most options and prevents your loan from becoming delinquent on your credit report.

Does paying extra each month always save money?

Paying extra toward principal reduces total interest paid, but aggressive payoff risks liquidity if it drains your emergency fund or leaves no cash buffer. Weigh accelerated payoff against maintaining enough savings to handle unexpected expenses without going into credit card debt.

Are there budgeting mistakes new graduates commonly make?

Many graduates neglect emergency savings or underestimate variable expenses, which causes their budgets to fall apart within a few months. Track your actual spending for at least 60 days before finalizing your budget, and revise it regularly as your income and expenses change.

Recommended

Comments